Thermal Energy Storage for Industrial Heat Decarbonization: Turning Renewable Variability into an Industrial Advantage

Thermal energy storage, industrial heat, decarbonization, electrification, renewable integration, flexibility, energy policy, Spain, Europe.

Alberto Toril Castro*

Papeles de Energía, N.º 32 (abril 2026)

Every factory needs heat – to cook, dry, melt, distill, sterilize, or shape the products we use every day. Industrial heat accounts for roughly two-thirds of all the energy that industry consumes, and it remains overwhelmingly dependent on burning fossil fuels on site. As renewable electricity scales across Europe and wholesale price volatility deepens, a new decarbonization pathway is gaining traction: converting surplus renewable electricity into storable heat for industrial use. This article examines the role of thermal energy storage (TES) in enabling that pathway. It defines industrial heat for a non-specialist audience, surveys decarbonization routes, and makes the case that TES offers distinctive system-level value through intraday price arbitrage, risk management, grid flexibility, and –critically– a structural reduction in Europe’s dependence on imported gas. The technology landscape is reviewed across sensible, latent, and thermochemical approaches, with particular attention to solid-media systems now entering commercial deployment. Rondo Energy’s experience is presented as an illustrative case. The article closes by identifying the regulatory and infrastructure barriers constraining deployment in Spain and Europe, and proposing a constructive policy agenda.

1. INTRODUCTION

Pedro Linares´ introduction to this issue covers the broader case for energy storage in the energy transition – the growth of variable renewables, deepening wholesale price volatility, and the systemic need for flexibility. This article takes that context as given and zooms in on a specific, massive, and surprisingly under-discussed challenge: decarbonizing industrial heat.

The numbers are staggering. According to the IEA, heat accounts for roughly half of all global final energy consumption and about 40 percent of energy-related CO₂ emissions. Half of that heat goes to industrial processes – close to 6 gigatonnes of CO₂ per year (IEA, 2019; 2023). In Spain, as in most of Europe, the great majority of this heat is still generated by burning natural gas, fuel oil, or coal on site. The power sector has been transformed by renewables over the past decade. Industrial heat has barely been touched.

The core argument of this article is that thermal energy storage can turn renewable variability from a liability into an asset for industry. Instead of forcing plants to consume electricity at the exact moment heat is needed, thermal storage decouples the grid draw from the heat delivery. Electricity gets converted into heat when it is abundant and cheap, stored efficiently, and dispatched as steam or hot air on demand – matching the plant’s process requirements while giving the grid a large, controllable, price-responsive load.

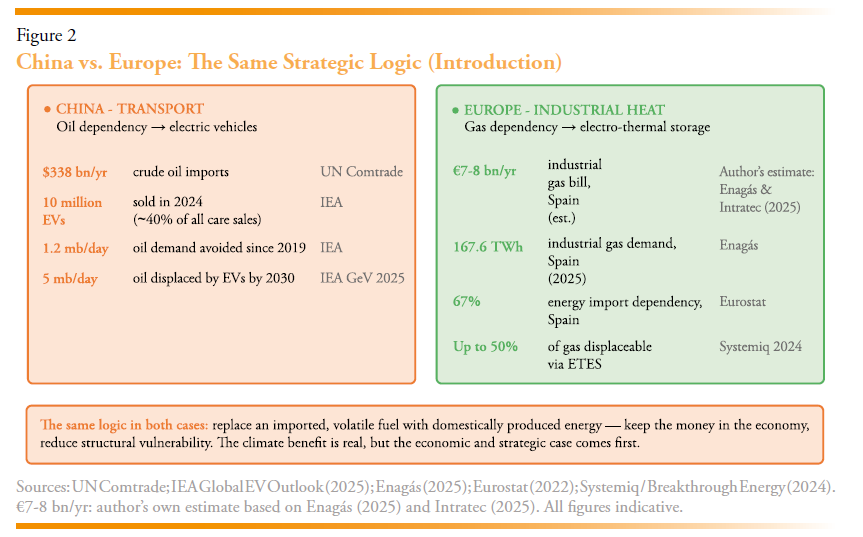

But this article is not just about emissions. It is about money, jobs, and strategic independence. Consider a parallel that is playing out in real time on the other side of the world.

China did not become the dominant electric vehicle market primarily because of climate policy. It did so because the country was spending over $338 billion per year importing crude oil –up from $20 billion just two decades earlier– creating a massive dependency on tanker routes through the Malacca Strait and on geopolitical relationships it could not fully control (UN Comtrade; IEA). The government responded by promoting battery-powered vehicles with extraordinary speed: in 2024, more than 10 million new energy vehicles were sold in China, accounting for roughly 40 percent of all new car sales. The IEA estimates that electric vehicles, LNG trucks, and high-speed rail expansion have together avoided oil demand growth of approximately 1.2 million barrels per day since 2019 – and that China’s consumption of gasoline and diesel actually declined for the first time in 2024 (IEA, 2025). By 2030, EVs are expected to displace more than 5 million barrels of oil per day globally, with China accounting for half of that reduction (IEA, 2025). The climate benefit is real, but the economic and sstrategic logic came first: replace an imported, volatile commodity with domestically produced energy, keep the money in the economy, and reduce a structural vulnerability.

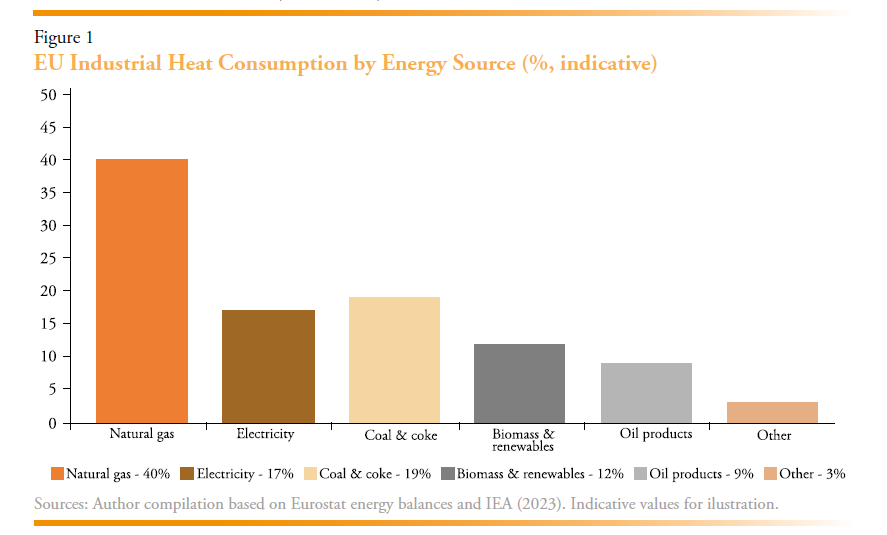

The scale of the challenge is visible in the numbers. As Figure 1 shows, fossil gas alone accounts for roughly 40 percent of European industrial heat supply today – with coal adding a further 19 percent. Electricity covers only 17 percent of demand, the vast majority of it in processes where direct resistance or induction heating has long been the only option. Biomass and renewables together account for around 12 percent, concentrated in sectors with abundant feedstock. The fuel mix has changed remarkably little over the past two decades, even as the power sector has been transformed.

Europe’s industrial heat challenge follows exactly the same pattern. The continent imports the vast majority of the natural gas its factories burn – from Norway, Algeria, the United States, Russia, Qatar, Nigeria, and others. Norwegian supplies, arriving by pipeline from a stable European partner, represent a partial exception to the geopolitical exposure; the rest does not. This creates a permanent outflow of capital, a structural exposure to price shocks (as 2022 and now 2026 demonstrated painfully [Ember, March 2026]), and a competitive vulnerability that no amount of hedging can fully eliminate. Every euro spent on imported gas to make steam is a euro that leaves the European economy. Electrifying industrial heat with domestically produced renewable electricity –stored in thermal batteries– reverses that flow. The fuel becomes local, the price becomes more predictable, and the money stays in the economy. What China is doing with cars and oil, Europe can do with factories and gas. Decarbonization is not the only reason to do this. It may not even be the most important one.

The article is organized as follows. Section 2 explains what industrial heat actually is – a topic less obvious than it sounds. Section 3 maps out the decarbonization options and positions TES among them. Section 4 describes how electro-thermal energy storage works and why it is different from electrical batteries. Section 5 reviews the main technology families. Section 6 walks through what real-world deployment looks like, drawing on Rondo Energy’s project experience. Section 7 digs into the barriers holding back scale-up in Spain and Europe. Section 8 sets out a policy agenda and closes with a forward-looking assessment.

Throughout this article, references to TES in an industrial electrification context refer specifically to electrically-charged systems –ETES– unless otherwise noted. The broader term TES is used where the argument applies to thermal storage as a general category.

I should note upfront that I write from a practitioner’s perspective – I work at Rondo and have been involved in project development across multiple geographies. That gives me a certain vantage point, but it also means the reader should expect me to be transparent about my perspective. Where Rondo is discussed, it is presented as one example in a growing market with over 40 ETES technology providers, not as the only game in town. My aim is analytical, not promotional.

2. The Overlooked Giant: What industrial heat is (and why it is hard to decarbonize)

2.1. A definition for non-experts

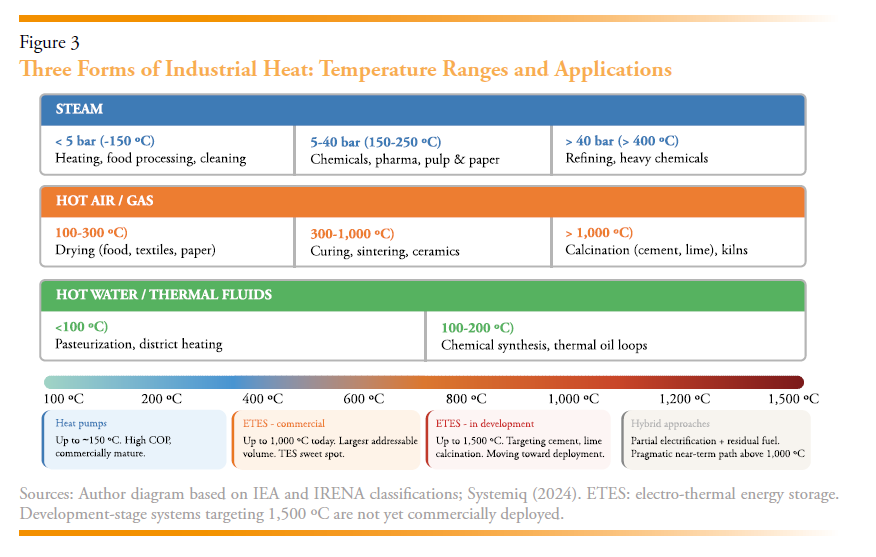

Industrial heat is simply the thermal energy used in manufacturing and processing. Not space heating, not domestic hot water – this is the heat consumed inside factories, refineries, and production facilities. If you have ever seen steam rising from a factory chimney, you have seen industrial heat at work. It is one of those things that is invisible in everyday life but absolutely fundamental to the economy: without industrial heat, there is no processed food on the shelf, no paper in the printer, no cement in the building, no steel in the car. It takes several distinct forms depending on the process.

Steam is the workhorse. It transfers heat, drives chemical reactions, sterilizes equipment, and provides mechanical energy through turbines. Broadly speaking, low-pressure steam (below 5 bar, around 150 °C) serves heating and food processing; medium-pressure steam (5-40 bar, roughly 150-250 °C) is the backbone of chemical, pharmaceutical, and pulp-and-paper operations; high-pressure steam (above 40 bar, past 400 °C) is needed for refining and heavy chemicals. A typical mid-sized plant can consume tens of tonnes of steam per hour, around the clock.

Hot air and hot gases are needed wherever a material must be in direct contact with a hot gas stream –drying paper, textiles, food products, or minerals; curing coatings; calcination and sintering in cement, lime, and ceramics. Temperatures range from 100 °C for gentle drying to well over 1,000 °C in kilns.

Hot water and thermal fluids serve pasteurization, district heating integration, and certain chemical syntheses – typically below 200 °C, though thermal oil systems can operate up to 300–350 °C in some industrial applications. These are typically the easiest to electrify.

2.2. Key sectors

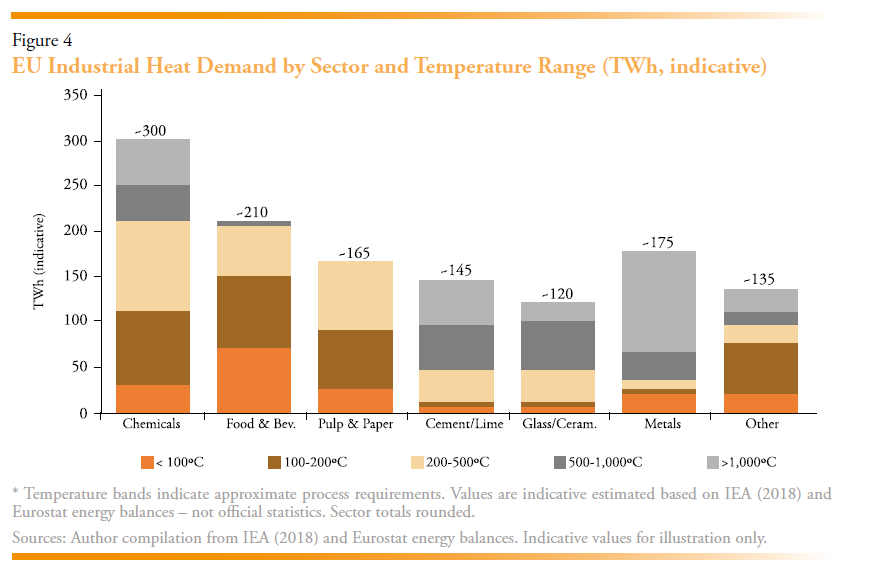

Across Europe –and Spain is no exception– industrial heat demand is concentrated in a handful of sectors. In Spain, the leading consumers of industrial gas are refining (around 20 percent), chemicals and pharmaceuticals (around 15 percent), food and beverage, and building materials (Enagás, 2024). The European picture follows the same hierarchy: chemicals and petrochemicals are the single largest consumer – massive quantities of steam for reactions, separations, drying. Food and beverage comes next: pasteurization, sterilization, cooking, drying, cleaning. Pulp and paper is extraordinarily heat-intensive –steam for pulping, drying, paper-machine operation. Building materials (glass, ceramics, bricks, cement) run high-temperature kilns and furnaces, often above 1,000 °C. Metals span moderate-temperature annealing through extreme-temperature smelting. And cement and lime production involves calcination at 1,400 °C or more – the outer edge of what current electrification technology can reach.

2.3. Temperature matters more than people think

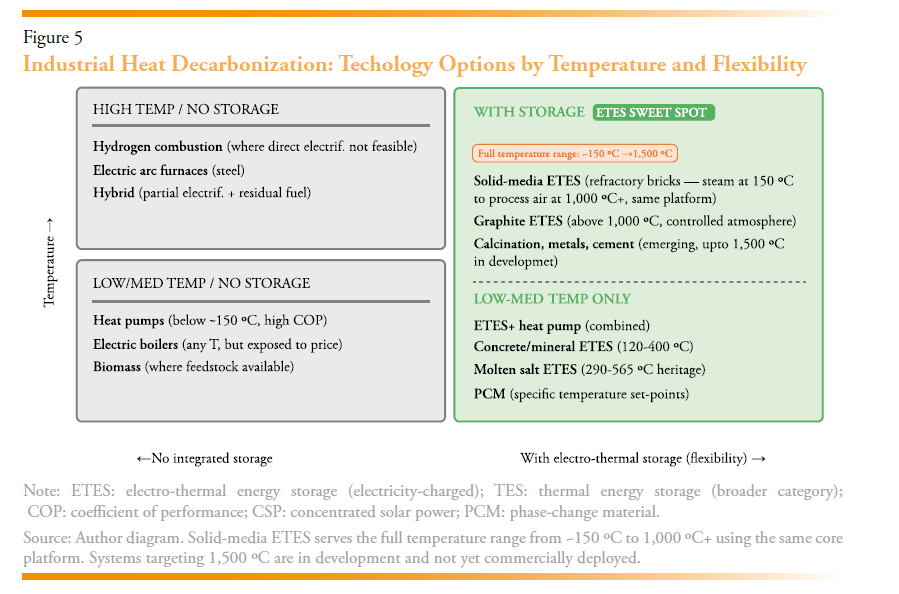

At the low end (below about 150 °C), heat pumps are increasingly competitive. The medium range (150-500 °C) is where the action is – the largest volume of fossil-fuel consumption, the biggest abatement opportunity, and the temperature band where TES has the strongest case. IEA data shows more than half of all industrial heat demand sits above 200 °C (IEA, 2018). Commercially available electro-thermal energy storage (ETES) systems can deliver up to 1000 °C today; systems designed for 1,500 °C are under development and moving toward commercial deployment (Systemiq & Breakthrough Energy, February 2024). Section 3 explains how these systems work and why they differ from conventional electrical batteries.

At the high end (above 500 °C, and often over 1,000 °C), options get thin. Electric arc furnaces handle steelmaking, induction heating covers some metallurgical jobs, but cement clinker, glass, and lime calcination remain tough to electrify at scale. Integrating electrification at these temperatures requires more R&D and engineering work, and solutions are actively in development. Some emerging approaches show near-term promise for parts of this segment. Broadly, hybrid configurations –partially electrifying what is feasible while retaining residual fuel for the rest– remain a pragmatic path for many operators in the near term.

The medium-temperature sweet spot deserves emphasis: largest addressable volume, commercially available technology, and the price band where electricity market dynamics matter most.

3. A simple map of industrial heat decarbonization pathways

3.1. The menu

There is no single silver bullet. The landscape is a menu, and each option has its conditions for viability.

Electric boilers are the most direct swap – replace gas with an electrode or resistance boiler. Mature, fast-responding, commercially available. The catch: zero buffering. The plant buys electricity at whatever the market charges, hour by hour. In most European markets today, the average price of electricity across all hours -including the morning and evening peaks, and overnight pricing- makes electrified steam uncompetitive with gas on a flat, continuous basis.

Heat pumps work well for low-temperature applications and are getting better every year. But the bulk of industrial steam demand at 150-400 °C remains beyond their efficient reach. High-temperature heat pump R&D is advancing, though commercial products above 200 °C are still rare. Where they can reach these temperatures, fundamentals prevent them from having a high coefficient of performance when serving these temperatures, unless they are able to tap into a waste heat source meaning the temperature lift is still manageable (e.g., <100 ºC). And like electric boilers, heat pumps offer no buffering: without storage, the plant still buys electricity hour by hour at whatever price the market sets. Their higher efficiency –a COP that can reach 2-4 at low temperatures but falls below 2 for steam generation applications above 150-200 °C– lessens the impact of that exposure but does not eliminate it.

Biomass boilers are proven in regions with abundant forestry residues – Scandinavia, parts of Central Europe. But feedstock is finite, competition for sustainable biomass is fierce (power generation, transport fuels, carbon removal all want it too), and scalability across the full volume of European industrial heat is not credible.

Renewable gases –biomethane and green hydrogen– get a lot of airtime. Biomethane is chemically identical to natural gas but severely supply-limited. Green hydrogen loses 30-40 percent of input electricity in the electrolysis step alone, faces unresolved infrastructure questions, and remains far more expensive than direct electrification for medium-temperature steam. For certain high-temperature niches where direct electrification cannot work, hydrogen may be essential. As a general-purpose solution for medium-temperature steam, it is hard to justify on physics or economics.

3.2. The volatility problem

Thermodynamically, direct electrification is elegant – resistance heating is close to 100 percent efficient. The problem is commercial. Plants need steam 24 hours a day. Electricity prices are discontinuous: cheap during hours of peak solar output, expensive in demand peaks (morning & evening), and often average (not cheap) overnight. The blended average across all hours still typically sits above gas.

But the gap is closing. In several European markets, day-ahead electricity is already cheaper than gas (including CO₂ charges) during 15-40 percent of hours, even after adding transmission and distribution charges (McKinsey & Company, March 2026). The problem is the remaining hours – the expensive ones pull the average back above gas parity for anyone who needs to buy electricity around the clock. This applies equally to electric boilers and heat pumps: both technologies are thermodynamically sound, but without storage they remain fully exposed to the price in every hour they operate. Higher efficiency reduces the bill; it does not change the structure of the problem.

3.3. TES as the missing piece

Thermal energy storage cracks this problem. The logic is simple: buy electricity during the cheap hours, convert it to heat, store it, and dispatch it when the plant needs it. ETES systems achieve 90-98 percent efficiency from grid electricity to stored heat (Systemiq & Breakthrough Energy, February 2024).

The economic effect: the plant’s effective electricity cost shifts from the blended all-hours average to a weighted average of only the cheapest hours. And here is the kicker – the deeper and more frequent the low-price windows (which is a direct consequence of more renewable capacity connecting), the better TES economics get. Renewables intermittency is not a problem for TES; TES is precisely designed to pair with such intermittency.

3.4. Complementarities

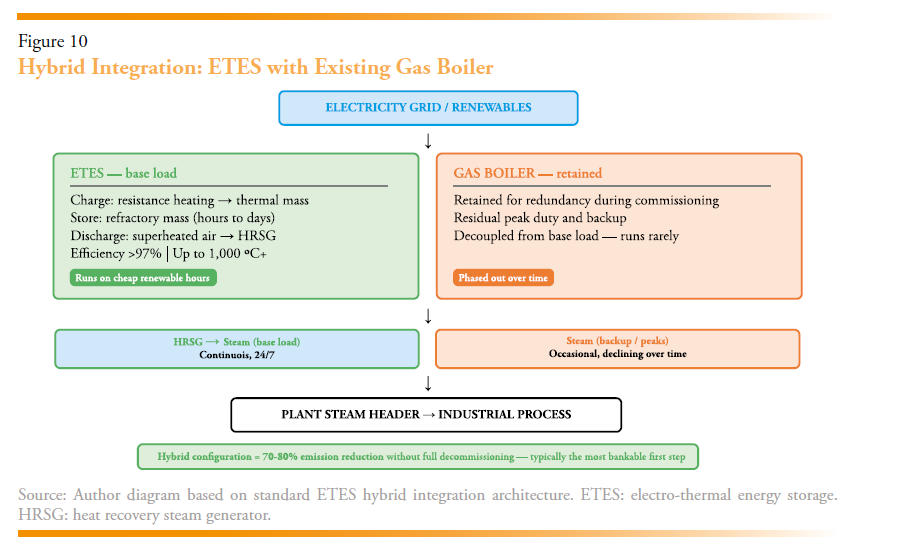

TES does not compete with other heat solution options – it enables them. A heat pump can serve the low-temperature loop while TES handles medium-temperature steam, at the same site. An e-boiler can back up a TES system. A hybrid system keeping a gas boiler for residual peak steam demand duty, and backup, while TES handles base load steam demand can cut emissions 70-80 percent without decommissioning anything – often the most bankable first step.

The way I think about it: TES is not a technology that displaces other technologies. It is the enabling layer that makes direct electrification work economically, by cutting the link between when electricity is consumed and when heat is delivered.

4. Electro-Thermal Energy Storage explained (and how it differs from batteries)

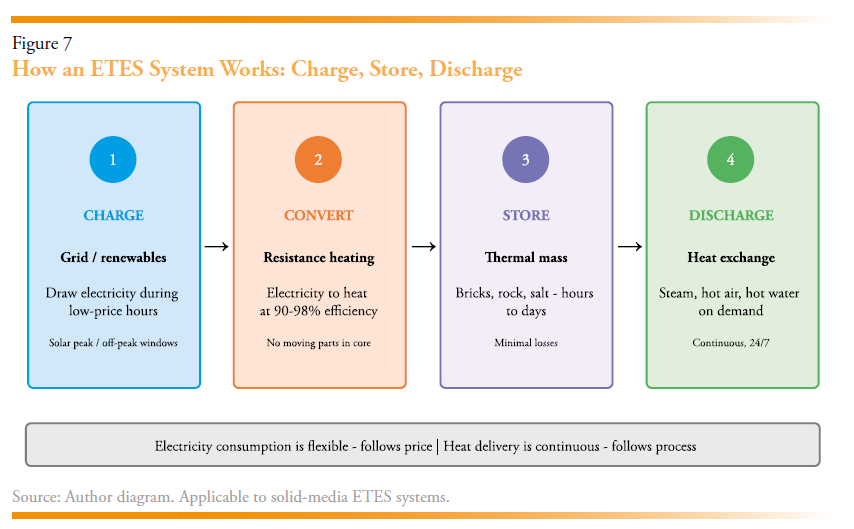

4.1. How it works

ETES systems share a common logic, but differ in storage medium, charging mechanism, and discharge configuration – as Section 5 describes in detail. The following describes the general principles, illustrated through solid-media refractory brick systems, which is the architecture this author knows best and which are furthest along in commercial deployment.

An ETES system does three things.

It charges: draws electricity during low-price hours and converts it to heat – typically using resistance heating elements, though some systems use direct Joule heating of the storage material itself.

It stores: the heat gets absorbed into a storage medium – bricks, rock, molten salt, others, depending on the technology (see Section 5 for a full review of storage families) – which holds the thermal energy for hours or days with minimal loss.

It discharges: when the plant needs heat, energy is extracted from the storage medium –through air or fluid flow, heat exchange, or direct radiative transfer, depending on the technology– and delivered as steam, hot air, or hot water at the required conditions. In solid-media refractory systems, discharge runs continuously and independently of the charging cycle; some other ETES architectures operate in cyclical charge/discharge modes.

Section 5 reviews the main storage media in detail –from refractory bricks and molten salt to phase-change materials– and explains the trade-offs between them

4.2. Why it is not a battery

The confusion with lithium-ion batteries is common and important to clear up. Think of it this way: a lithium-ion battery is like a rechargeable bank account denominated in electricity – you put electricity in, you get electricity out. If what you actually need is heat, you then have to take that electricity and run it through a heater – an extra step, with extra equipment and extra cost. An ETES system stores energy as heat from the outset, and returns it as heat. The conversion step still exists –for steam applications, a heat exchanger or steam generator is needed on the discharge side; for hot air applications, heat is delivered directly– but in either case it is the same equipment the plant already operates. The more fundamental difference is economic: storing energy as heat in refractory bricks or rock costs a fraction of storing it as electricity in lithium-ion cells. Since the end use in a factory is heat, storing it in that form avoids a round-trip through electrochemical storage and back – and that round-trip is where both cost and efficiency are lost.

This has several practical consequences. The storage materials bricks, rock, sand- are dirt cheap and available everywhere in the world. There are no rare or critical minerals involved (no lithium, no cobalt, no nickel). Capital costs per unit of stored energy for grid-scale batteries can be more than double those for ETES (Systemiq & Breakthroug Energy, February 2024). And from the electricity grid’s perspective, ETES provides something different from batteries: instead of storing electricity and releasing it back to the grid at peak times (which is what batteries do), ETES creates a large, flexible electricity consumer that absorbs surplus renewables during the cheapest hours. Both functions help the system. In the case of ETES, this is sector coupling –connecting the heat energy system to the electricity energy system– and using storage in the heat energy system to provide very large volumes of demand-side flexibility into the electricity system, which is exactly what the system needs as it integrates more intermittent renewable generation.

4.3. System-level value

4.3.1. The Spain opportunity in numbers

Before getting into the value stack, it is worth pausing on the scale of the opportunity in Spain specifically, because the numbers are larger than most people realize.

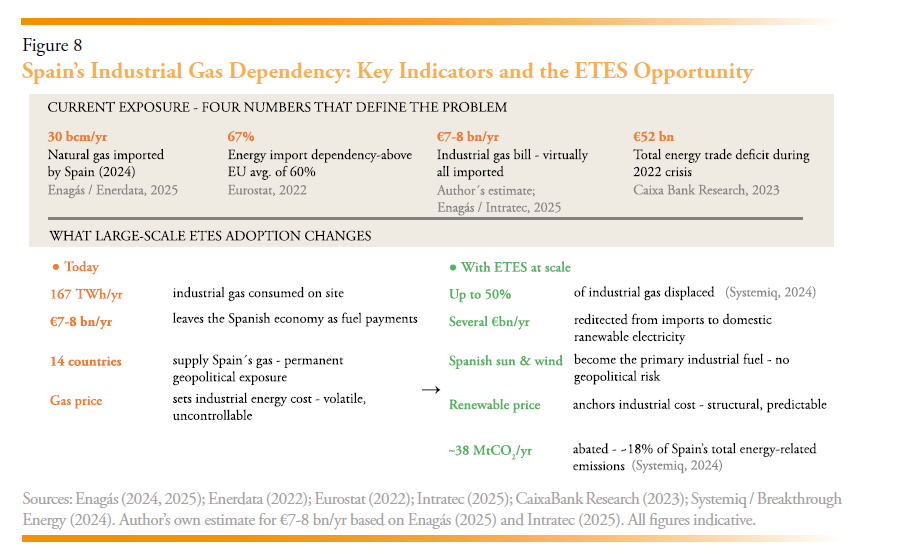

Spain imported approximately 30 billion cubic metres of natural gas in 2024, arriving from 14 different countries – mainly Algeria (39%), Russia (21%), the United States (17%), and Nigeria (14%) (Enagás, 2024; Enerdata, 2025). Domestic gas production is negligible – roughly 540 GWh in 2023, less than one percent of consumption. Spain’s energy import dependency ratio sits at approximately 67 percent, above the EU average of 60 percent (Eurostat, 2022).

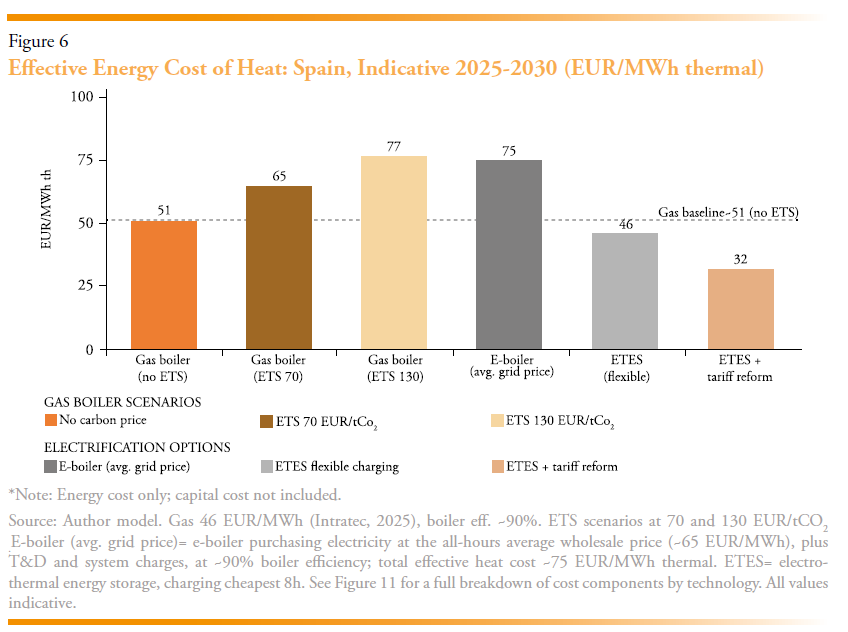

Of the total gas consumed domestically, industry is the single largest consumer. Industrial gas consumption in Spain reached 167.6 TWh in 2025, even after a 5.2 percent decline driven mainly by lower cogeneration output (Enagás, 2025). As noted in Section 2, demand is concentrated in refining, chemicals, food and beverage, and building materials – the same sectors that account for the bulk of decarbonization potential. The industrial gas price in Spain stood at around 46 €/MWh in early 2025 (Intratec, 2025).

What does this mean in money? At that price level, Spanish industry’s gas bill for heat alone runs in the estimated range of €7-8 billion per year – virtually all of it spent on imported fuel, flowing out of the Spanish economy. During the 2022 energy crisis, Spain’s gas trade deficit reached €22 billion in a single year, and the total energy deficit hit €52 billion – roughly 4 percent of GDP (CaixaBank Research, 2023). Even in calmer years, the structural outflow is enormous. And unlike the cost of a solar panel –which you buy once and then generate free fuel for 30 years– the gas bill arrives every single month, at whatever price the global market dictates that week.

Meanwhile, on the electricity side, Spain’s renewable transformation has been dramatic. Renewables accounted for 58 percent of electricity production in 2024, and over the course of 2025 Spain consistently ranked among the European markets with the lowest wholesale electricity prices – with 44 percent of hours below 14 €/MWh and an annual average of around 65 €/MWh (Ember, 2025; CNMC, 2025). An Ember analysis found that solar and wind capacity added in the past five years avoided 26 billion cubic meters of gas imports worth €13.5 billion – almost five times what Spain invested in its transmission grid over the same period (Ember, 2025). The critical caveat is that wholesale prices are only part of what industry actually pays: once transmission charges, system levies, and taxes are added, the all-in cost can be two to three times higher – a structural distortion that Section 7 addresses directly.

The paradox is that this cheap, abundant renewable electricity is largely unavailable to industry for heat – because industrial plants cannot stop and start their boilers with the sun and wind, and because the grid, tariff, and regulatory infrastructure for industrial electrification has not caught up with the generation transformation. TES is the bridge between the two: it lets industry access the cheap renewable hours for heat production, without sacrificing the continuity that manufacturing demands.

The potential is correspondingly large. Systemiq and Breakthrough Energy estimate that large-scale ETES adoption in Spain could displace up to 50 percent of the country’s current gas consumption and abate around 38 million tonnes of CO₂ –equivalent per year– roughly 18 percent of Spanish energy-related emissions (Systemiq & Breakthroug Energy, February 2024). That is a shift of several billion euros per year from imported fossil fuel to domestically generated renewable electricity – strengthening energy security, improving the trade balance, and anchoring industrial competitiveness in a structural cost advantage rather than a commodity bet. The logic is the same as China’s electric vehicle push, applied to factories instead of cars: replace an imported, volatile fuel with a domestic, increasingly cheap one. The emissions reduction is a consequence, not the cause.

4.3.2. The four layers of value

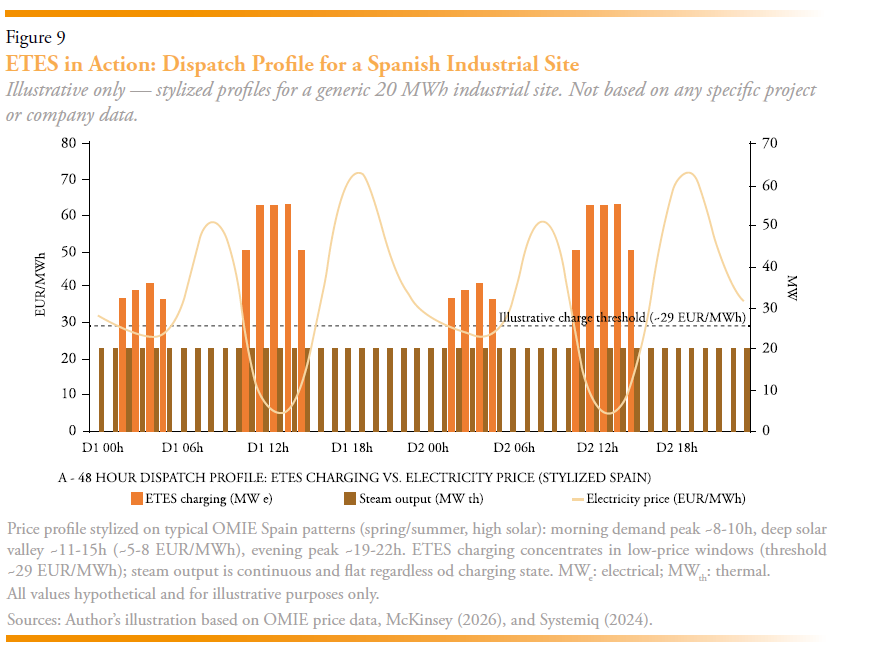

Within-day arbitrage – the most visible layer. In Spain, midday solar surpluses already produce multi-hour windows of very low prices on most days. The spread between those hours and morning and evening peaks is material and widening. Further overnight electricity prices are typically higher than cost of gas.

Risk management. An ETES-equipped site hedges simultaneously against gas prices and carbon prices. By converting cheap renewable electricity into stored heat, the plant reduces exposure to gas-price swings and to the EU ETS allowance trajectory. For a CFO signing off on a 15-year capital investment, that dual hedge matters.

Grid value. Because ETES charging concentrates in off-peak, high-renewable hours, peak demand can drop 6-30 percent versus flat electrification scenarios (Systemiq & Breakthroug Energy, February 2024). In Spain, ETES on industrial sites could add roughly 4 GW of controllable off-peak demand by 2030 – a serious contribution to absorbing solar surpluses and relieving congestion.

Investor economics. McKinsey’s modelling of eight-hour ETES systems across six European countries finds projected IRRs above 15 percent in most markets under 2030 conditions. Spain comes out on top, above 20 percent (Mckinsey & Company, March 2026). Across Europe, the cumulative investment opportunity is estimated at around €16 billion as ETES capacity scales from under 0.5 GWh today to over 200 GWh by 2035.

4.4. New business models

The commercial landscape is also shifting. Heat-as-a-service (HaaS) models are emerging, where rather than the industrial customer buying or leasing an ETES system, they buy heat (often in the form of steam). To deliver this, one player (e.g., ETES provider) will install and finance the ETES system, buy electricity, and combine the two to sell heat to the industrial customer at a contracted €/MWh. This takes the capital investment, electricity trading complexity, and performance risk out of the equation for the industrial. The industrial simply buys an energy commodity (heat). For industrial companies that do not have an energy trading desk or do not want to invest in non-core assets or ETES technology, the HaaS commercial structure makes the economic benefits of ETES accessible (Mckinsey & Company, March 2026).

5. The main families of Thermal Storage: Options and trade-offs

This section gives a non-technical overview of the technology landscape. The goal is not to pick winners but to give the reader a map of the options and the dimensions along which they differ. All the information captured here represents only publicly available data.

5.1. Sensible heat – solids

This is the broadest and most commercially advanced category, encompassing several distinct architectures.

Refractory brick systems use structured arrays of ceramic bricks heated by electrical resistance elements. The same aluminosilicate ceramics have a long track record in high-temperature industrial applications — notably in steelmaking blast stoves (Cowper stoves) operating at up to 1,500 °C with 30-year service lives. The DLR characterizes these systems as drop-in boiler replacements with high efficiency and safety (DLR, 2026).

Graphite-based systems can reach very high temperatures (above 2,000 °C). Because graphite is susceptible to oxidation above certain temperatures, these systems generally require controlled-atmosphere containment – an engineering consideration that adds system complexity and influences facility integration requirements. Several companies are developing graphite-based thermal batteries targeting both industrial heat and thermophotovoltaic electricity generation.

Packed bed and granular media systems (rock, sand, ceramic spheres) are attractive for their low material costs. As with all sensible heat systems, outlet temperature declines during discharge as the thermal front progresses through the storage medium; in unstructured beds this effect is more pronounced and typically requires additional heat management downstream, though it is manageable from a system design perspective. The DOE and Sandia have documented multiple pilot and demonstration projects using packed beds for industrial heat applications (DOE, 2023).

Concrete and mineral systems with embedded heat exchangers store heat in concrete or volcanic-rock blocks. Charging and discharging can be achieved via embedded steel pipes carrying thermal oil or steam, though some mineral systems use other heat transfer configurations. They typically operate in a moderate temperature range (around 120–400 °C). Thermo-mechanical management –controlling thermal ramps and ensuring compatibility between any embedded piping and the surrounding medium– is a key design consideration for long-term durability. Several European companies have brought modular concrete TES systems to commercial deployment.

5.2. Sensible heat – liquids

Molten salt systems (typically nitrate-based) have track records from concentrated solar power, with roughly 50 GWh deployed globally across multiple CSP installations. Proven operating range is approximately 290-565 °C. The upper limit is set by the thermal stability of conventional nitrate salts, while the lower bound reflects the need to keep the salt above its solidification temperature (~220 °C), which requires continuous heat tracing. The technology is mature at TRL 7-9 for solar-charged configurations. The adaptation of molten salt storage to electrically charged industrial ETES configurations is an active area of development, with several companies working on commercial systems. Research into next-generation salt chemistries (e.g. chloride salts) aims to raise the temperature ceiling, though these remain at earlier development stages (IRENA, 2020; NREL, various).

5.3. Latent heat (PCM)

Phase-change materials exploit the energy absorbed or released during melting and solidification. PCM systems offer higher energy density per unit volume than sensible-heat systems, which is an advantage in very highly space-constrained environments. The main engineering challenges include low thermal conductivity of many PCM materials (which limits charge/discharge rates), potential for material degradation over many cycles, and the complexity of encapsulation at industrial scale.

5.4. Thermochemical

Reversible chemical reactions offer the highest theoretical energy densities and the possibility of long-duration or even seasonal storage with minimal thermal losses. Challenges related

to reaction kinetics, material stability, and system complexity have so far limited deployment to

laboratory and pilot scale (IRENA, 2020). Active research continues, and the technology may become relevant at longer time horizons, but it is not yet at commercial deployment stage for industrial heat applications.

5.5. Why solid-media systems are gaining ground in industry

Among the options, solid-media sensible-heat systems –and particularly refractory brick architectures– have moved fast toward industrial deployment. The reasons are practical: materials are globally abundant (aluminosilicate bricks are made from aluminium, silicon, and oxygen – together about 80 percent of Earth’s crust); architecture is simple, with no moving fluids, no freeze risk, and minimal degradation; service life can exceed 30 years, based on proven analogues in high-temperature industrial applications; storage costs sit at the lower end of the ETES spectrum; energy efficiency is high (90-97+%).

The slight trade-off is footprint – a solid-media system takes up somewhat more space per unit of stored energy than a PCM or thermochemical system. However, in vast majority of industrial sites, including in urban locations in Europe, enough space exists on-site, often even next to the existing boiler house. This is a manageable constraint. In very heavily space-constrained environments, other solutions may be more appropriate.

6. From concept to reality: What deployment looks like in industrial sites

6.1. Rondo as an illustrative case

There are over 40 ETES technology providers globally (Systemiq & Breakthrough Energy, February 2024). I focus on Rondo here because it is the system I know best. The integration challenges and lessons are broadly representative of solid-media ETES deployment.

The Rondo Heat Battery stores energy in free-standing arrays of refractory bricks. Inside the unit, the brick stack is organized as a checkerboard of open chambers, with electrical resistance heating elements suspended within them. The key insight is in how the heat gets from the heater to the brick. Rather than blowing hot air over the bricks (which is how most heating systems work), Rondo’s heaters transfer energy directly through thermal radiation – the same way the sun warms your face, or a campfire heats you from across the room. The physics of radiation (described by the Stefan-Boltzmann law) means that in an enclosed chamber, all surfaces that can “see” each other rapidly reach the same temperature. Rondo’s design approach enables standard, off-the-shelf industrial heating elements to bring the bricks to much higher temperatures than would be possible with convective heating. A key engineering challenge in radiative systems –managing hot spots and thermal stress on the storage medium– is addressed through the system’s chamber geometry and heating element configuration.

During discharge, air flows through channels between the hot bricks and comes out superheated – at temperatures above 1,000 °C. The superheated air exiting the bricks then runs through a heat-recovery steam generator (HRSG) –a standard piece of industrial equipment in combined-cycle power plants– to produce steam at whatever pressure and temperature the industrial plant needs. The system is not limited to high-temperature operation or steam delivery. The same core platform can deliver heat across a wide range – from steam at 150°C for food processing to superheated air above 1,000°C for calcination. Output temperature is controlled by adjusting airflow and the downstream delivery configuration. A plant requiring medium-pressure steam at 250°C uses the same bricks and heating elements as one requiring 900°C process air – only the HRSG specification and duct configuration change.

Electricity-to-delivered-heat efficiency is above 97 percent. The system can deliver superheated air above 1,000 °C – temperatures required for hard-to-abate sectors such as alumina and cement.

6.2. Integration lessons from the field

A few observations that apply to solid-media refractory brick ETES systems – the focus of this section – though many apply more broadly:

Retrofit beats greenfield for near-term deployment. Most projects today are retrofits – ETES installed alongside an existing gas boiler at an operating plant. The gas boiler provides redundancy. A hybrid solution, running ETES for base load and gas for “top-up” in days when there are fewer (e.g., <6) hours of cheap electricity, can cut site emissions 70-80 percent and provides the overall cheapest cost of heat. For many industrial firms, this is the step they are willing to take.

Grid connection is a bottleneck. The most common source of delay across European projects is not the ETES technology but the process of securing adequate electricity grid connection. Sites that have run on gas for decades typically lack the 10-50 MW electrical connection needed for ETES. Upgrading involves multi-year timelines, permitting, and sometimes uncertainty. In Spain, timelines for connection queues for large industrial loads are a well-documented issue.

Operations are simple. No chemical reagents, no moving parts in the storage core, no freeze protection, no inert atmospheres. Materials are non-combustible and non-toxic. Charge is managed by optimization software running against electricity price forecasts. Discharge of heat is “on-demand” and operators familiar with conventional boilers need only modest training as the discharge controls are highly similar. These characteristics apply to solid-media refractory systems; Some other ETES systems have different operational considerations, as noted in Section 5.

Heat demand certainty is a financing asset. Industrial heat demand is well-characterized – plants know their steam profiles in detail. This predictability, in contrast to the weather-dependent uncertainty of renewable generation, allows ETES projects to be structured around long-term heat-supply agreements with predictable revenue. Bankable, boring revenue streams.

6.3. Across sectors and geographies

ETES projects span food and beverage, chemicals, aluminium, biofuels and fuels, and building materials across geographies including the US, Europe, Africa, and Asia. The variety of applications drives home an important point: any industrial site with significant steam or hot-air demand and access to the electricity grid could potentially benefit from ETES. The same core Rondo platform serves everything from food-processing steam at 150 °C to hot air above 1,000 °C. Only the downstream delivery subsystem changes (HRSG for steam, direct air duct for high-temperature process heat, or turbine integration for co-generation). Every deployment in any sector adds operating hours and performance data to a shared experience base, which accelerates bankability for the next project.

A few sector-specific observations are worth drawing out.

Food and beverage. This is often the first sector where ETES projects reach financial close, for a straightforward reason: steam requirements are moderate in temperature (typically 150-200 °C), demand profiles are well-characterized and relatively flat, and the sites tend to have some available footprint. The sustainability commitments of large food companies –driven by both Scope 1 reporting and consumer-facing brand pressure– create internal pull for electrification. The challenge is usually grid capacity, not process integration. A food-processing plant switching a 15 MW gas boiler to ETES may need an electrical connection upgrade that takes longer to secure than the ETES installation itself.

Chemicals and pharmaceuticals. Chemical plants use steam at a wide range of pressures and temperatures, often with multiple steam headers at different conditions. ETES systems can be configured to feed into one or more headers. The key learning from chemical-sector projects is that the plant’s steam balance –how much steam is generated, consumed, and vented across different process units– must be mapped in detail before sizing the ETES system. In complex chemical sites, getting the steam balance right is a precursor to sizing the ETES system.

Aluminium and metals. Alumina refineries need large volumes of steam for the Bayer process (digestion of bauxite) and very high-temperature heat for calcination of aluminium hydroxide at 950-1,000 °C. The calcination step has historically been considered unreachable by electrification. A refractory ETES system delivering superheated air above 1,000 °C can serve both the steam requirements and integrate with calcination, from the same core platform – the downstream delivery subsystem changes but the storage and charging system is identical. This “one platform, multiple applications” characteristic is strategically significant for aluminium producers evaluating full-site decarbonization pathways.

Cement and lime. These sectors present the most demanding temperature requirements – clinker production involves calcination at temperatures approaching 1,400 °C and above. While commercially deployed ETES systems have not yet reached these extreme temperatures, active development work –supported by government R&D grants in multiple countries– is targeting the adaptation of calciners to operate on superheated air from ETES, or CO₂ used as a heat-transfer medium. The cement sector represents both the toughest technical challenge and, if solved, one of the largest single-sector abatement opportunities in European industry.

Co-generation and power. In some configurations –particularly for industrial sites with sizeable heat load and steam needs at or below 20 bar– ETES can feed high-pressure steam (e.g., 100 bar) through a turbine to generate electricity and extract lower-pressure steam (e.g., 20-bar) from the turbine to meet the process heat need. There is additional capital investment for this configuration: steam turbine, additional electricity connection and storage capacity. The benefit is that the baseload electricity served from the system, is from a system that is drawing in electricity from the grid during the cheapest hours. That electricity arbitrage can create material value in the right market conditions. The system further benefits that the energy storage is far cheaper than li-ion energy storage, and the system maintains >95% energy efficiency as both the electricity and heat output from the turbine are used.

7. What blocks scale today in Spain and Europe – and what would unlock it

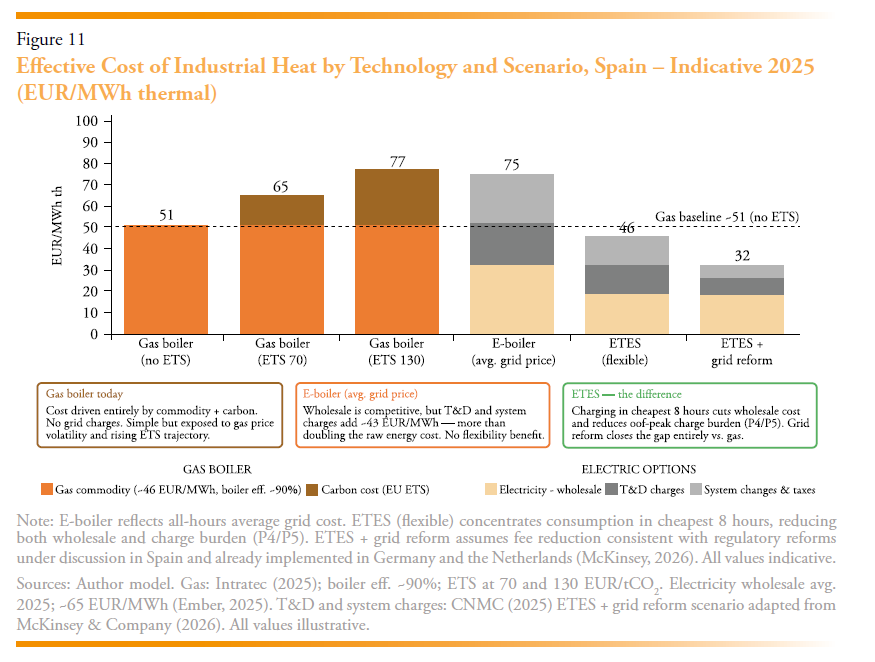

The technologies are commercially available. The economy is moving in the right direction – though the picture is more nuanced than a simple “electrification is now cheaper than gas.” As Figure 11 illustrates, the wholesale electricity price is only part of what industry pays: once grid charges, system levies, and taxes are added, the all-in cost of electrified heat remains competitive with gas in the cheapest hours but not across the board. In markets with high renewable penetration like Spain, McKinsey modelling suggests IRRs above 20 percent for flexible ETES by 2030, but today, under current tariff structures and without grid fee reform, the margin is tighter than the headline numbers suggest. European deployment still lags far behind its potential. The obstacles are not technological – they are regulatory, infrastructural, and institutional. Closing that gap is primarily a policy challenge.

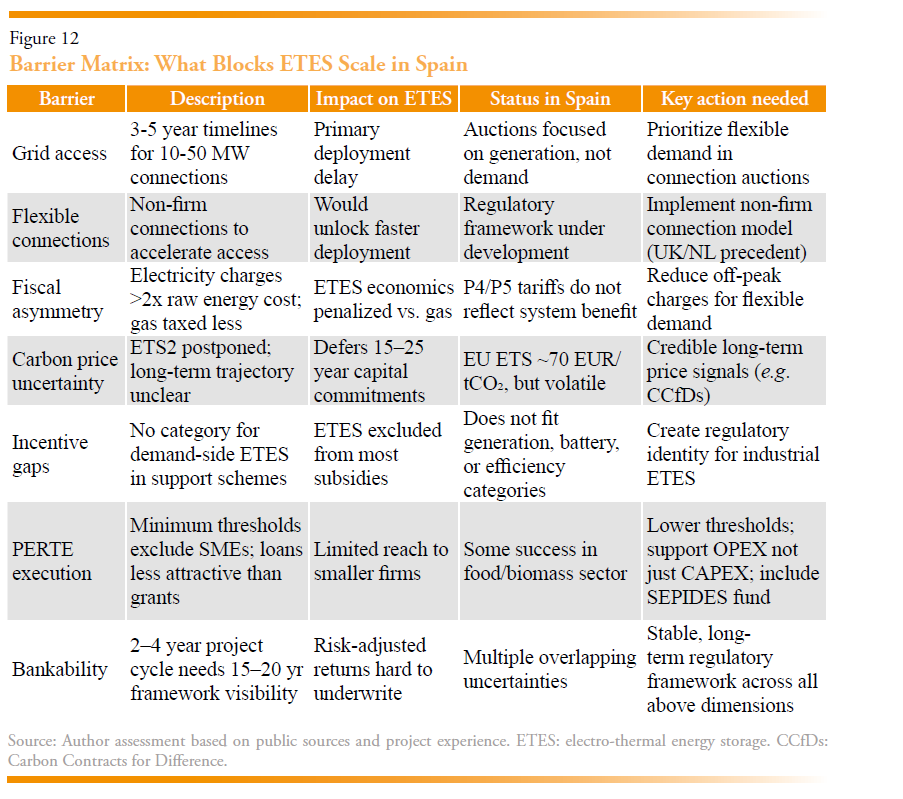

7.1. Grid access

The most immediate barrier. A mid-sized plant switching from gas to ETES may need 10-50 MWe of connection capacity. In Spain and across much of Europe, getting this capacity can take three to five years or more, with real uncertainty about timing, cost, and technical feasibility.

Grid-connection auctions in Spain have focused mainly on generation projects. Industrial demand, even flexible demand from ETES -that would only consume during off-peak hours when there is spare capacity in the existing network and relieve renewables curtailment by consuming during surplus hours- has not been prioritized in the past. Projects that would help the grid are queued behind projects that create congestion. There is no prioritization with network benefits in mind.

7.2. Flexible connections

One promising approach: non-firm or flexible connections, where an industrial consumer agrees to cap its grid draw during system-stress hours in exchange for faster, cheaper access during the majority of hours when capacity is available. The Entra Coalition is pushing this model in Spain, and precedents already exist in the UK, Germany and the Netherlands.

The regulatory framework in Spain is still under development. The RDL 7/2026 establishes the legal basis for flexible grid access for demand-side storage installations in Spain (RDL 7/2026), introducing the principle that storage permits need not guarantee supply in all hours of the year. The framework now exists; what remains pending is the CNMC’s development of specific conditions and their practical application to industrial ETES sites.

7.3. Electricity costs versus gas costs: The fiscal tilt

There is a persistent structural disadvantage, and its nature is precise: the system charges and taxes layered on top of the wholesale electricity price are disproportionately high relative to the equivalent burden on gas. Gas pays for its fuel and, increasingly, for its carbon emissions through the EU ETS. Electricity pays for its fuel plus transmission, distribution, system charges, and multiple levies that collectively can more than double the raw wholesale cost.

What matters for an industrial decision-maker is not the wholesale price of electricity in isolation, but the all-in cost of consuming a megawatt-hour of heat from each source – and that comparison, illustrated in Figure 11, looks very different depending on the technology and electricity consumption conditions. A flat e-boiler, buying power around the clock at average grid electricity cost remains uncompetitive with gas in most scenarios today. An ETES system charging flexibly in the cheapest hours closes most of that gap. This asymmetry does not reflect the actual network system costs and environmental cost of the two routes – it actively penalizes the cleaner option (consuming electricity outside of demand peaks, during solar generation peak output). Reforming tariff structures -reducing charges during off-peak periods (P4/P5 in the Spanish system) to reflect the system benefit of flexible demand- would directly improve ETES economics and correct a distortion that has no justification on either efficiency or environmental grounds. Electricity networks are sized to meet peak demand. Highly flexible electricity demand (e.g., from ETES) adds zero electricity demand to the peak. It uses the existing network when it is otherwise underutilized. For the network, this means more MWhs of electricity demand without any required network investment, drastically improving network utilization.

7.4. Carbon price uncertainty

The EU ETS gives a carbon-price signal that in theory favours electrification. But industrial firms making 15-25 year investment decisions need a credible trajectory, not a spot price. The postponement of ETS2 and ongoing political debates about allowance reductions have injected uncertainty. When the carbon price outlook is unclear, capital commitments to electrification get deferred.

7.5. No home for demand flexibility

Most European support mechanisms target supply-side technologies – renewable generation, grid-scale batteries, hydrogen production. There is a notable absence of mechanisms that reward large flexible industrial electricity demand or behind-the-meter thermal storage. ETES does not fit existing categories: it is not generation, not a grid battery, not a traditional efficiency measure. Giving it a clear regulatory identity and ensuring eligibility for relevant support would remove a needless barrier.

7.6. Spain: PERTE programmes and industrial hesitation

Spain has created specific instruments for industrial decarbonization through its PERTE programmes. The PERTE for industrial decarbonization has had some success – particularly in the food sector using biomass. But the instruments often do not reach small and medium enterprises due to minimum investment thresholds, and loan-based support is less attractive than grants. The bigger question is what comes after PERTE funding runs out. One potential answer is already taking shape: the SEPIDES decarbonization fund, launched to provide long-term financing for industrial transition projects, could fill part of that gap – provided its instruments are structured to support OPEX as well as CAPEX, and that ETES is explicitly included as an eligible technology category.

More broadly, there is a “first-mover hesitation” problem. Technologies are available and economics are improving, but companies keep deferring decisions because they lack confidence in the stability of the regulatory framework -grid tariffs, carbon prices, subsidy eligibility- over the lifetime of the asset. For most industrial firms the critical variable is not CAPEX but OPEX: the investment decision follows from the operational-cost outlook, and without long-term visibility on energy costs, capital does not move.

7.7. Bankability requires predictability

Replacing a gas boiler with TES involves engineering studies, procurement, grid applications, permits, and often board-level capital approval (though capital approval not necessary in the case of storage-as-a-service or heat-as-a-service). The whole process can take two to four years before construction starts. For the investment to be financeable, the framework needs to be stable and visible over 15-20 years.

That is not today’s reality in most European markets. Grid access uncertainty, fiscal ambiguity, carbon-price volatility, and shifting subsidy rules create an environment where the risk-adjusted returns -attractive in a spreadsheet- are hard to underwrite in practice. Solving this is not about better technology. It is about better policy.

8. Conclusion: Thermal Storage as an enabler of flexible, electrified industrial heat

8.1. A constructive agenda

The barriers in Section 7 are real but not immovable. Six reforms, taken together, would substantially change the picture.

- 1. Faster, clearer grid connections. Accelerate build-out for industrial demand. Recognize flexible demand (including ETES) in connection auction frameworks as a system asset – it reduces curtailment and congestion, not just adds load.

- 2. Flexible connections. Implement a regulatory framework for non-firm industrial connections, drawing on UK and Dutch models and the Entra Coalition’s work in Spain.

- 3. Rebalance electricity taxation. Reform tariffs so off-peak charges (P4/P5) reflect the actual system benefit of consuming outside of demand peaks and during high-renewable hours. Stop penalizing electrification relative to fossil-fuel combustion through an outdated fiscal structure.

- 4. Flexibility remuneration. Allow industrial thermal storage to participate in balancing mechanisms, capacity markets, and ancillary services. Create explicit pathways for behind-the-meter ETES.

- 5. Stable long-term signals. Give industrial firms credible 15-20 year visibility on carbon prices, electricity market design, and support mechanisms. Instruments like Carbon Contracts for Difference (Richstein et al., 2024) offer one model for de-risking these investments.

- 6. Accessible support instruments. Make PERTE and successor programmes accessible to smaller firms. Support OPEX, not just CAPEX. Include electro-thermal storage explicitly as an eligible technology category. Consider European-level coordination to avoid asymmetries between member states.

8.2. Where this leaves us

Industrial heat decarbonization is one of the biggest remaining pieces of the energy transition and one of the least visible to the general public. The technology to address a large share of this challenge –electro-thermal energy storage– exists today, is commercially deployed, and is increasingly competitive.

Spain, with world-class solar resources, electricity price volatility, and a large industrial heat base, has some of the most favourable conditions for ETES deployment in Europe. The McKinsey and Systemiq analyses point to IRRs above 20 percent (Mckinsey & Company, March 2026) and abatement potential equivalent to almost a fifth of the country’s energy-related emissions (Systemiq & Breakthrough Energy, February 2024). These projections are not speculative: McKinsey’s modelling covers six European markets under 2030 electricity and carbon-price assumptions, with Spain consistently ranking first on return potential.

What is missing is not technology. What is missing is a regulatory and market framework that matches the ambition of the technology with the predictability that industrial capital demands. The reforms outlined above are neither radical nor untested – most have close analogues in existing European energy policy. Their implementation would allow Spain to cut industrial emissions, bring down industrial energy costs, absorb more renewable generation, and position itself as a competitive, low-carbon manufacturing destination.

The strategic dimension should not be lost in the technical detail. Europe spends tens of billions of euros per year importing fossil gas to heat its factories. That money leaves the continent, feeds price volatility, and creates dependency on suppliers whose interests do not always align with Europe’s. Every industrial boiler that switches from imported gas to stored renewable electricity is a small act of energy independence – a factory that will never again be disrupted by a pipeline dispute, an LNG price spike, or a geopolitical crisis in a producing country. China understood this logic for transport and acted on it: 10 million electric vehicles sold in a single year, 1.2 million barrels per day of avoided oil demand, a $338 billion annual import bill finally bending downward. Europe has the same opportunity for industrial heat, and arguably better starting conditions: world-class renewable resources, mature electricity markets, established industrial infrastructure, and a manufacturing base that is actively looking for answers. The question is whether policy will move fast enough to let it happen.

Renewable variability is usually talked about as a problem. For industrial heat, thermal energy storage turns it into a resource. The next phase of the transition depends on letting that happen – not on paper, but at the scale and pace the climate demands.

Notes

* Rondo Energy.

References

Agora Energiewende, & Agora Industry. (2023). Transforming Industry Through electricity.

Cabeza, L. F. et al. (2021). Thermal energy storage – overview and specific insight. Energy.

CaixaBank Research. (February 2023). Spain’s energy trade deficit in figures.

CNMC. (2025). Reports on grid access and connection regulation in Spain.

Columbia University SIPA & Center on Global Energy Policy (CGEP). (2025). China’s Oil Demand, Imports and Supply Security. May.

DLR. (2026). Thermal Energy Storage Handbook.

Ember. (2025). Decoupled: How Spain cut the link between gas and power prices using renewables. October.

Ember. (2026). Latest energy shock reminds Europe of its risky gas reliance. March.

Enagás. (2024). Distribution of industrial natural gas consumption in Spain in 2023, by sector [Graph]. Statista. https://www.statista.com/statistics/1320902/industrial-natural-gas-consumption-share-by-sector-spain/

Enagás. (2024–2025). Demand for natural gas in Spain [Annual press releases].

Enerdata. (2025). Spain energy information.

Entra Coalition. Position papers on flexible industrial connections.

ENTSO-E. Transparency Platform: Generation, curtailment, cross-border flow data.

European Commission. EU ETS Directive and ETS2 regulatory framework.

Eurostat. (2022). Energy balances – industry sector detail.

Henry, A., Prasher, R., & Majumdar, A. (2020). Five thermal energy grand challenges for decarbonization. Nature Energy.

IEA. (2018). Industrial Heat Demand by Temperature Range.

IEA. (2019). Renewables 2019: Heat.

IEA. (2023). Energy System Overview: Industry.

IEA. (2025). Oil Demand for Fuels in China has Reached a Plateau [Commentary].

IEA. (2025). Global EV Outlook 2025. May.

IEA. World Energy Outlook. Latest edition.

Intratec. (2025). Natural Gas Price in Spain.

IRENA. (2020). Innovation Outlook: Thermal Energy Storage.

LDES Council. (2023). Net-zero heat: LDES to accelerate energy system decarbonization.

McKinsey & Company. (2024). Net-zero electrical heat: A turning point in feasibility. July.

McKinsey & Company. (2024). Tackling heat electrification to decarbonize industry. December.

McKinsey & Company. (2026). Industrial heat electrification in Europe: New business models emerge. March.

MITECO. (2023). Plan Nacional Integrado de Energía y Clima (PNIEC).

NREL. Various publications on molten salt thermal energy storage.

Olympios, A. V. et al. (2023). Technology options for thermal energy storage. Applied Energy.

OMIE. (2023–2025). Annual market reports.

Real Decreto-ley 7/2026, de 20 de marzo, por el que se aprueba el Plan Integral de Respuesta a la Crisis en Oriente Medio. Boletín Oficial del Estado, núm. 71, 21 de marzo de 2026.

Red Eléctrica de España. El sistema eléctrico español. (Latest edition).

Richstein, J. C., et al. (2024). Catalyzing the transition to a climate-neutral industry with carbon contracts for difference. Joule, 8(12), 3233–3238.

Systemiq, & Breakthrough Energy. (2024). Catalysing the Global Opportunity for Electrothermal Energy Storage. February.

Systemiq, & Breakthrough Energy. (2024). Country Memo: Spain. February.

U.S. DOE. (2023). Thermal energy storage technology strategy assessment (OE0038).