Fecha: july 2025

Santiago Carbó-Valverde*, Pedro Cuadros-Solas** y Francisco Rodríguez-Fernández***

Abstract

Low-income households are typically financially vulnerable, yet some exhibit overconfidence in their financial knowledge, potentially leading to risky financial behavior. This paper explores the Dunning-Kruger-like effect in personal finance among low-income individuals in Spain, examining whether those with the least financial knowledge are the most overconfident and how this overconfidence relates to risky financial decisions. Using survey data on Spanish households’ financial behaviors and literacy, we measure objective financial knowledge and self-assessed financial confidence to construct a “confidence gap.” We find evidence that low-income respondents with poor objective knowledge often significantly overestimate their financial abilities. Overconfident individuals (those with high confidence but low literacy) demonstrate a greater self-reported tolerance for risk and are more likely to engage in potentially risky financial behaviors such as high-cost borrowing. These results are robust in regression and machine learning analyses controlling for income, age, and education. The findings suggest a considerable behavioral bias: financially vulnerable groups not only lack knowledge but fail to recognize that lack, which may exacerbate their exposure to financial risks. We discuss policy implications, recommending targeted financial education and behavioral interventions to improve decision-making in low-income populations. Strengthening financial literacy and calibrating individuals’ self-awareness of their knowledge limitations are vital steps to protect vulnerable households and foster more prudent financial behavior.

1. INTRODUCTION

Household financial decision-making often deviates from classical rational models due to cognitive biases and limited knowledge. One pervasive bias is overconfidence – the tendency to overestimate one’s own skills or knowledge. In the context of personal finance, overconfidence can be especially detrimental for low-income households, who have little margin for financial error. Low-income individuals generally display lower objective financial literacy (Lusardi & Mitchell, 2014) and may at the same time exhibit unwarranted confidence in their financial acumen. This combination of low competence and high confidence evokes the classic Dunning-Kruger effect (Kruger & Dunning, 1999), where those with the least ability are often unaware of their deficits and thus overestimate their proficiency. We posit that such “financial overconfidence” among low-income households can lead to risky financial behaviors – for instance, taking high-interest loans, not diversifying savings, or failing to anticipate economic shocks – ultimately undermining their financial stability.

Prior research has documented that overconfidence plays a significant role in financial decision-making. Overconfident investors trade excessively and take on more risk, often to their detriment (Barber & Odean, 2001). In personal finance, confidence in one’s financial knowledge can be miscalibrated: many individuals lack fundamental financial skills yet remain confident in their ability to manage money (Lusardi & Tufano, 2015). For vulnerable groups, this miscalibration is particularly concerning. Low-income households tend to have lower financial literacy on average – e.g., fewer than half of Spaniards could correctly answer basic interest and inflation questions in national surveys (Bover et al., 2018) – yet they are not always aware of these knowledge gaps. International studies find that financial literacy is lowest among those with less education and income, who also disproportionately rate their financial skills as “good” or “average” (OECD, 2020). This suggests that the least financially knowledgeable may not accurately perceive how much they don’t know.

The Dunning-Kruger effect provides a theoretical lens: individuals with low ability in a domain lack the metacognitive skills to recognize their own incompetence, resulting in inflated self-assessments (Kruger & Dunning, 1999; Dunning, 2011). Applied to financial behavior, a low-income person with poor understanding of interest rates or budgeting might confidently believe they are making sound decisions, inadvertently taking on excessive debt or foregoing precautions like savings and insurance. Recent work by Samanez-Larkin et al. (2020) indeed found that an overestimation of financial knowledge was associated with greater risk tolerance in older adults, suggesting overconfident individuals are more willing to engage in risky financial behaviors. Similarly, a study in Japan provocatively asked “Is financial literacy dangerous?” after observing that people with higher financial literacy sometimes became overconfident and took on more debt and investment risk than advisable (Kawamura et al., 2020). These findings highlight a crucial nuance: improving financial knowledge is vital, but if it breeds overconfidence without true competence, it could backfire and encourage recklessness (Vörös et al., 2021).

This paper makes an original contribution by connecting these insights to the context of low-income households. While overconfidence in financial matters has been studied among investors and the general population, there is a research gap in focusing on the financially disadvantaged. Low-income individuals often face precarious conditions and limited buffers, so the consequences of financial misjudgments can be severe (Lusardi et al., 2011). Understanding whether overconfidence exacerbates their vulnerability is key for designing effective interventions. We use new survey evidence from Spain to examine (1) the extent of financial overconfidence in a low-income sample, and (2) whether such overconfidence correlates with risky financial behavior. Spain provides a relevant case given its efforts to improve financial literacy in recent years and the persistent socioeconomic disparities in financial outcomes. By studying Spanish low-income households, we gain insights applicable to other settings where financial fragility and limited literacy are concerns.

The remainder of the paper is organized as follows. The next section reviews the literature on financial literacy, overconfidence, and household financial behavior, with a focus on low-income populations. We then describe our data and methodology, including the construction of a “confidence gap” measure (self-perceived knowledge minus actual knowledge) and indicators of risky financial behavior. The Results section presents our empirical findings: we visualize the distribution of confidence gaps, illustrate the relationship between actual and perceived financial knowledge, and report regression and machine learning analyses linking overconfidence to behavior. A Discussion follows, interpreting the results and highlighting policy implications for financial education and consumer protection targeted at vulnerable groups. The final section concludes and suggests avenues for future research.

2. Literature Review

2.1. Financial Literacy and Low-Income Households

Financial literacy – the knowledge and skills to manage personal finances – is widely recognized as a key determinant of sound financial behavior (Lusardi & Mitchell, 2014). Individuals with greater financial literacy are more likely to budget, save for emergencies, participate in prudent investments, and avoid high-cost debt, whereas those lacking basic knowledge often make suboptimal decisions that impair their financial well-being (Lusardi & Tufano, 2015). Unfortunately, numerous studies document that financial literacy is lowest among low-income and less-educated groups (Atkinson & Messy, 2012; OECD, 2020). Low-income households frequently cannot correctly calculate interest payments, understand inflation, or grasp concepts like risk diversification. This knowledge gap contributes to outcomes such as low retirement savings, higher use of high-interest credit, and difficulty navigating financial products. For example, in Spain’s 2016 Survey of Financial Competences, only 58% of adults correctly answered a basic inflation question and 46% correctly answered a compound interest question, with success rates significantly lower among those with primary education or in the bottom income quartile (Bover et al., 2018). These disadvantaged households are also more likely to be financially “fragile,” lacking the savings to cope with income shocks (Lusardi et al., 2011). Improving financial literacy in low-income communities is therefore a policy priority to promote financial inclusion and reduce vulnerability.

2.2. Overconfidence and the Dunning-Kruger Effect

Overconfidence is a well-documented cognitive bias in which individuals’ subjective confidence in their judgments exceeds their objective accuracy. In classic experiments, people often rate their abilities as “above average,” a statistical impossibility (Brown, 2012). Kruger and Dunning (1999) famously demonstrated that those with the least skill in domains like humor, grammar, or logic grossly overestimated their performance – an effect attributed to metacognitive deficits. Lacking knowledge, they are also short of the awareness of what competence in the domain looks like, leading them to mistakenly believe they are doing well. Conversely, highly competent individuals may slightly underestimate themselves, in part because they assume tasks that are easy for them are easy for others (Dunning, 2011). This asymmetric miscalibration – large overestimation at the bottom end and modest underestimation at the top end – is the hallmark of the Dunning-Kruger effect.

In financial settings, overconfidence manifests in multiple ways. One stream of research in behavioral finance has examined overconfidence among investors, finding it can lead to excessive trading and risk-taking. Barber and Odean (2001) showed that overconfident investors (proxied by, e.g., male traders who typically are more confident in financial matters) traded more frequently and earned lower net returns due to transaction costs. Overestimation of one’s stock-picking skill or knowledge of the market can result in under-diversified portfolios and optimistic risk assessments. Overconfidence is also implicated in the underestimation of downside risks – investors may believe they can time the market or avoid crashes, which can amplify bubbles and subsequent losses.

Beyond investments, everyday financial behaviors can also suffer from overconfidence. A consumer might overestimate their understanding of mortgage terms and sign a complex loan they cannot afford, or be too confident that they can manage high credit-card debt, only to fall into a debt spiral. Overconfidence in financial knowledge has been linked to lower demand for advice or information – those who think they already know enough may be less likely to seek help from financial counselors or to read the fine print of financial products (Mitchell & Curto, 2010). Notably, recent research by Samanez-Larkin et al. (2020) found that among older adults, an objective-subjective knowledge mismatch (i.e., overconfidence) was associated with greater self-reported willingness to take financial risks, even though actual risk aversion behaviorally did not always increase. This suggests that overconfident individuals perceive less risk or feel more emboldened to take risks. Similarly, overconfidence can lead to susceptibility to fraud – overconfident consumers might assume they can’t be duped by scams and therefore fail to take precautions (Xia et al., 2021).

2.3. Financial Overconfidence in Low-Income Populations

Low-income individuals are not typically active stock traders, but overconfidence can influence their financial choices in more everyday contexts. For example, a low-income household might overestimate its ability to repay a high-cost payday loan or be overly optimistic about avoiding fees and penalties when juggling bills. Bertrand and Morse (2011) noted that cognitive biases, including overoptimism about one’s finances, contribute to repeated payday loan borrowing. Overconfidence may also deter low-income persons from seeking financial education or advice – they might believe they are handling their finances well enough, when they are incurring avoidable costs (such as overdraft fees or high interest charges).

Research directly examining overconfidence among low-income or less-educated groups is relatively sparse, which is where our study contributes. However, tangential evidence comes from financial education studies: sometimes individuals with a little financial training can develop a false sense of security. Kawamura et al. (2020), in an analysis titled “Is Financial Literacy Dangerous?”, found that in Japan higher financial literacy was paradoxically associated with some risky attitudes – people with more knowledge reported greater willingness to take financial risks and, in some cases, held more debt, suggesting that education without complementary self-awareness might lead to overconfidence. These findings imply that as financial literacy initiatives reach low-income communities, they should be designed carefully to avoid instilling unwarranted confidence. The forms of financial literacy overconfidence can vary – some people overestimate their knowledge of specific topics (like inflation) while recognizing gaps elsewhere, whereas others broadly overrate their financial savvy (Vörös et al., 2021). Each form can differently impact financial well-being. Our study targets a broad form: the general confidence a person has in their overall financial understanding relative to their actual literacy.

2.4. Risky Financial Behavior

We define “risky financial behavior” in this context as actions or decisions that expose households to high levels of financial risk or stress. Examples include: taking on high-interest debt without a repayment plan, not maintaining an emergency savings cushion, investing in speculative schemes or fraudulent scams, and failing to insure against common risks. For low-income households, even spending beyond one’s monthly income (without backup funds) constitutes risky behavior, as it can trigger a cycle of borrowing or arrears. Indeed, one survey found a significant fraction of Spanish households regularly spend more than their income and must resort to borrowing from family, using credit, or running down assets to cope (Bover et al., 2018). Such coping strategies can be risky if they rely on unsustainable sources (e.g., expensive credit or depleting limited savings).

Prior literature suggests that financial literacy is inversely related to many risky behaviors. For instance, more financially literate individuals are less likely to over-indebt themselves or fall for predatory loans (Lusardi & Tufano, 2015). However, as noted, if higher literacy breeds complacency or overconfidence, this protective effect could be offset. Some studies highlight gender or cultural differences in confidence affecting risk behaviors: for example, women on average report lower financial confidence and also tend to be more financially conservative (investing less in risky assets), whereas men’s higher confidence corresponds with more risk-taking (Chen & Volpe, 2002; Barber & Odean, 2001). The implication is that confidence (whether justified or not) can be a driver of behavior independently of actual knowledge.

3. Variable- vs. Fixed-Rate Mortgages in Spain

Based on the literature, we test two main hypotheses:

(H1) Financial overconfidence is present among low-income households, particularly those with low objective literacy – i.e., a Dunning-Kruger-like pattern where the least knowledgeable individuals have relatively high self-assessed knowledge.

(H2) Overconfidence is associated with riskier financial behavior in low-income households – those who overestimate their financial capability will be more prone to behaviors like borrowing beyond their means, foregoing budgeting, or choosing high-risk financial products (relative to their wealth level). The null hypothesis for H2 would be that actual knowledge (or other factors) fully explains behavior, with overconfidence adding no predictive power. Our analysis will evaluate these hypotheses using detailed survey evidence from Spain.

This study uses microdata from a national survey conducted by Funcas jointly with The Cocktail consulting in March 2025. The survey specifically targeted the financially vulnerable population in Spain and was designed to explore their access to, use of, and attitudes toward formal and informal financial services. A total of 1,003 individuals aged 18 to 65 were surveyed using stratified sampling techniques to ensure representation across gender, age cohorts, and regions. The questionnaire includes both subjective and objective measures of financial literacy. Subjective knowledge was self-assessed on a 1-to-5 scale, while objective knowledge was captured through three standard questions on inflation, interest rates, and risk diversification. In our analytic sample, the median annual household income is around €20,400, and we classify 27% of respondents as low-income (household income roughly below €18,000). While our analysis emphasizes this low-income subgroup, we include the full sample for certain comparisons to highlight differences by income level.

The survey included a battery of financial literacy questions covering fundamental concepts such as inflation, interest rates, and risk diversification. Each respondent’s objective financial knowledge is assessed by their performance on these quiz questions. We construct an index of objective literacy by summing scores across 14 knowledge questions. Each question was scored on a 0–10 scale (reflecting correctness and confidence, as described below), yielding a total knowledge score ranging from 0 to 140 points for each individual. In our sample, the mean knowledge score is about 70.3 (out of 140), indicating roughly 50% of the maximum possible – this aligns with prior findings that the average person correctly answers about half of standard financial literacy questions (Bover et al., 2018). There is wide variation: some respondents scored near zero (essentially no correct knowledge) while a few achieved close to full marks. We interpret higher scores as greater financial literacy.

Crucial to our analysis is the subjective side of financial knowledge. The survey asked respondents to self-assess their financial knowledge. Specifically, each individual rated their overall financial knowledge on a scale from 1 (“very low”) to 5 (“very high”). This self-rating provides a measure of perceived financial capability or confidence. The average self-rating in our sample is about 2.9 out of 5, with the majority (roughly 47%) rating themselves “3” (moderate knowledge). Notably, self-assessed knowledge is only weakly correlated with actual quiz performance (Pearson’s r ≈ 0.10), suggesting substantial miscalibration – many respondents who scored low on the quiz still gave themselves middling or high knowledge ratings, and vice versa.

From these two components, we derive our key variable of interest: the financial confidence gap. We define the confidence gap for each individual as:

Confidence Gap = (Self-rated knowledge, standardized) − (Objective knowledge, standardized).

In practice, to make the scales comparable, we convert the 1–5 self-rating to a percentage (0%–100%) and the objective score to a percentage of total points, then take the difference. A positive confidence gap indicates that a person’s self-assessed knowledge is higher than their actual knowledge would warrant (overconfidence), while a negative gap indicates underconfidence. For ease of interpretation, one can also think in terms of population percentiles: who rates themselves in a higher percentile of knowledge than their tested performance percentile.

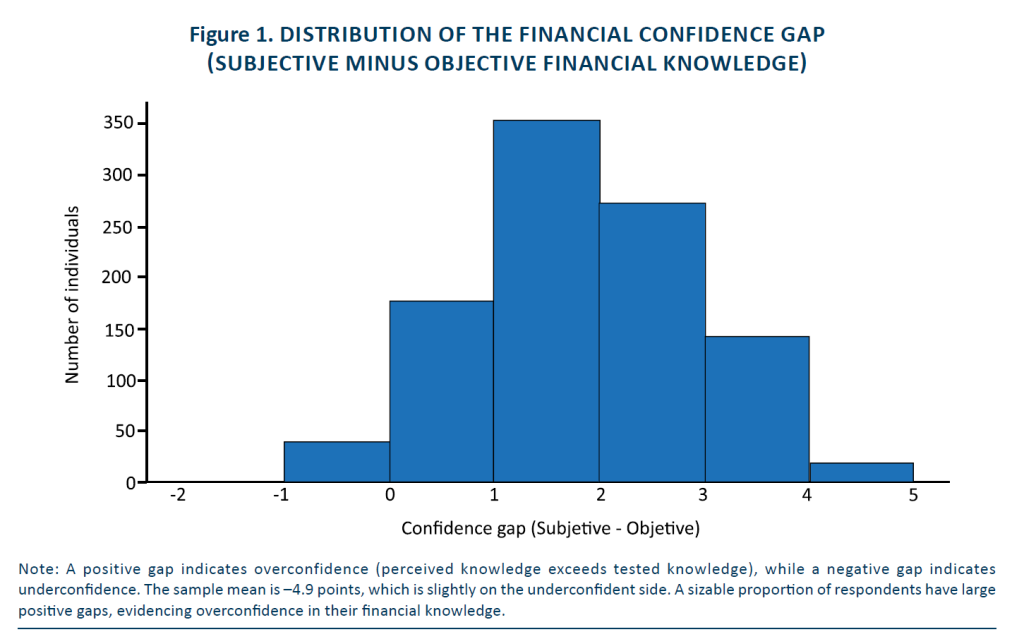

On average, the confidence gap in our sample is slightly negative (mean ≈ –5 points on a 0–140 scaled difference, equivalent to about –4.9 on the 0–100% scale), implying a slight overall tendency toward underestimation of knowledge. However, this average masks a very skewed distribution. Figure 1 shows the distribution of confidence gaps across individuals. Most respondents cluster near a gap of zero (self-perception roughly in line with actual knowledge), but there are long tails on both sides. A substantial subset exhibits large positive gaps (overconfidence), some by over +50 points, and another subset shows large negative gaps (underconfidence). We note that 36% of the total sample can be classified as overconfident (self-rating above their actual knowledge quartile), 38% as underconfident (self-rating below their actual quartile), and only about 23% as well-calibrated (self-rating matches their knowledge quartile). These statistics already hint at a Dunning-Kruger pattern – if people were perfectly self-aware, we would expect a much higher calibrated percentage.

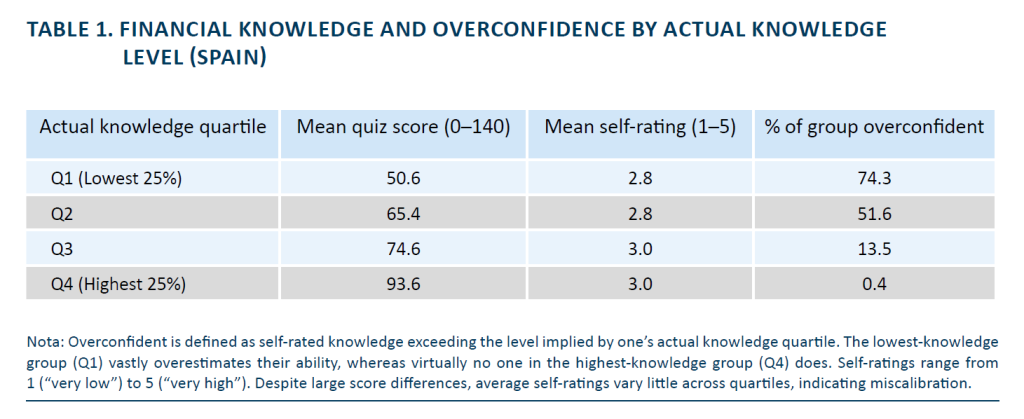

How does this miscalibration relate to actual knowledge level? To investigate the Dunning-Kruger effect, we rank individuals by their objective knowledge and examine their average self-assessments. Table 1 summarizes objective and subjective knowledge by quartiles of actual financial literacy. Strikingly, the lowest knowledge group (bottom 25% in quiz score) still rated their financial knowledge at 2.8 out of 5 on average – the same self-rating that the second quartile gave, and not far below the 3.0/5 average of the top quartile. In fact, over 74% of individuals in the bottom knowledge quartile were overconfident (their self-rating exceeded what their knowledge score would predict), and virtually none of the top quartile were overconfident (most were correctly calibrated or underconfident). This clearly illustrates a Dunning-Kruger type pattern: the least knowledgeable are largely unaware of their deficiencies and rate themselves similarly to far more knowledgeable peers. Meanwhile, the most knowledgeable group does not massively overrate themselves – if anything, some underrate their relative expertise (only 0.4% of the top quartile were overconfident, with many rating “3” despite high scores, perhaps assuming the questions were easy for everyone). Thus, our data confirm a systematic confidence gap inversely related to actual competence.

We also examine differences by income group within our sample. Low-income respondents (bottom ~27%) had slightly lower objective knowledge scores on average (around 68 points) than higher-income respondents (71 points), and they also self-rated slightly lower (2.81 vs. 2.90). Interestingly, the incidence of overconfidence was higher among the low-income group – about 40% of low-income individuals were overconfident, compared to 34% of those with higher incomes. This aligns with the notion that disadvantaged groups both know less and are somewhat more likely not to realize it. However, in both groups a sizeable one-third or more exhibit overconfidence, confirming that miscalibration is not unique to any income stratum. We therefore proceed to analyze the consequences of financial overconfidence for behavior, with particular attention to the low-income segment.

The survey also collected data on various financial behaviors, such as borrowing habits, saving, and product usage. We constructed several indicators of potentially risky or suboptimal behavior for analysis:

- Spending > Income (and coping mechanisms): Respondents were asked whether in the past year their household expenditures exceeded income, and if so, how they covered the shortfall. Options included drawing down savings, borrowing from friends/family, taking out a loan (or using credit card debt), selling assets, or simply not paying some obligations. We define a risky coping indicator equal to 1 if a respondent who faced an income shortfall resorted to any form of borrowing (formal or informal) or missed payments, as opposed to covering the gap through savings or adjusting expenses. This measure reflects behavior that could lead to financial stress (e.g., taking high-interest loans or accruing arrears). In our sample, about 69% of households had an episode of overspending in the last year; the majority of those used at least one risky coping strategy (borrowing or delaying bills). This high figure underscores the precarious position of many households, especially low-income ones.

- High-Cost Credit Use: Using data on loan sources, we flag individuals who reported using “fast loans” or financing companies (often high-interest lenders) or credit cards to cover everyday expenses. Only a small fraction (under 5%) explicitly mentioned resorting to payday-type loans (“préstamos informales”), likely due to stigma or low access in Spain. However, around 28% borrowed from family or friends (an informal safety net), and ~22% used consumer credit or credit card debt to manage shortfalls. Relying on such means regularly can be considered risky for low-income households, as it may lead to debt accumulation.

- Lack of Emergency Savings: We observe whether respondents had any form of precautionary savings. Not having an emergency fund (even a small one) is risky because any shock will necessitate borrowing or cutting essential consumption. A sizable share of low-income respondents reported they could not come up with even €1,000 in an emergency, indicating high vulnerability.

- Risky Asset Investment: Although not common among low-income individuals, we check whether respondents invested in volatile assets (e.g., equities or cryptocurrencies). In our sample, only about 4% owned stocks and 6% had cryptocurrency or similar speculative investments. Interestingly, those who did engage in such investments tended to have slightly higher literacy scores, but also higher self-confidence; for instance, stock owners had an average self-rating of 3.3 versus 2.93 for non-owners, despite similar knowledge scores, hinting at a role of confidence in the decision to invest. For low-income investors, such investments can be risky if they do not fully understand them or cannot afford potential losses.

- Financial Planning Behavior: We also consider behaviors like budgeting, comparison shopping for financial products, or seeking financial advice. Not engaging in basic planning or information gathering can be risky by omission. The data show that a significant portion of respondents do not use budgets or keep track of expenses, which can lead to inadvertent overspending.

From these various measures, we construct a composite “risky financial behavior” index for use in regression analysis: it equals 1 if a respondent engaged in any of the following in the past year – took out high-cost loans, borrowed from family/friends to cover basic expenses, fell behind on debt payments or bills, or had no savings and overspent income. While this index combines multiple dimensions, it captures the general notion of financially precarious behavior. In our sample, approximately 69% fell into this category (as noted, overspending and borrowing were prevalent). We will analyze this as an outcome variable in relation to overconfidence and other factors.

4. Methodology

Our empirical strategy integrates econometric and machine learning approaches to examine the association between financial overconfidence and risky financial behavior among economically vulnerable individuals in Spain. This mixed-methods design enables both hypothesis testing and pattern discovery.

4.1. Descriptive Exploration

We begin with a descriptive analysis of the key variable of interest: the confidence gap, defined as the difference between an individual’s subjective self-assessment of financial knowledge (on a 1–5 scale) and their objective score on three financial literacy items (scored 0–3). Positive values reflect overconfidence, while negative values indicate underconfidence.

We examine how this gap varies across observable characteristics—such as gender, age group, migrant status, and income level—to test the Dunning-Kruger hypothesis (H1): individuals with lower objective knowledge tend to exhibit inflated confidence. These initial analyses provide visual and statistical support for the hypothesized miscalibration and motivate the multivariate modeling that follows.

4.2. Logistic Regression Models

To formally assess the relationship between overconfidence and risky financial behavior (H2), we estimate a series of logistic regression models of the following form:

logit(P(Ri=1))=β0+β1Gapi+β2Ki+β3Incomei+β4Xi+εi

Where:

- Ri is a binary indicator equal to 1 if individual ii engaged in any of the following high-risk behaviors: cryptocurrency use, direct stock investment, or borrowing from informal lenders.

- Gapi is the confidence gap.

- Ki is the objective financial knowledge score.

- Incomei is a dummy for low household income (defined in the lowest tercile of the national income distribution).

- Xi is a vector of control variables: gender, age group, migrant status, and education level.

We also estimate alternative specifications replacing the gap with an overconfidence dummy (1 if the gap > 0), and we interact this dummy with the low-income indicator to test whether the effect of overconfidence is stronger among financially vulnerable individuals.

All regressions apply survey sampling weights and cluster standard errors at the respondent level (each representing a distinct household). Model fit is evaluated using the Hosmer–Lemeshow test, pseudo R-squared, and AIC/BIC criteria. Marginal effects at means are computed for interpretability.

This modeling framework allows us to distinguish between the effect of knowledge per se and the miscalibration of knowledge, isolating whether it is the overestimation of ability (rather than ignorance alone) that correlates with risk-taking.

4.3. Drivers of Housing Investments

To assess the robustness of our results in a model-agnostic framework and to uncover nonlinear interactions, we complement the regressions with two supervised classification models:

- A Decision Tree Classifier using the CART algorithm, and

- A Random Forest Classifier with 100 trees.

The dependent variable remains the same (binary indicator of risky behavior). Predictors include the confidence gap, financial knowledge, low-income status, gender, age group, and migrant status. For the Decision Tree, we constrain the tree depth to 3 to enhance interpretability and avoid overfitting. This produces a sequence of binary splits revealing the most salient thresholds and interactions between predictors. The resulting tree provides a transparent decision rule for identifying high-risk individuals based on their profiles. The Random Forest is trained using a 75/25 train-test split and the Gini impurity criterion. We do not tune hyperparameters extensively, as our primary objective is interpretability and robustness. We report:

- Variable importance scores, which reflect the average reduction in node impurity attributable to each predictor;

- Accuracy, precision, recall, and F1-score on the test set;

- and the ROC-AUC score as a summary measure of discriminative performance.

Importantly, the Random Forest allows us to verify whether the confidence gap consistently emerges as a top predictor of risky behavior in a flexible, nonlinear setting—validating our regression findings through an alternative lens.

4.4. Limitations and Robustness

Our analysis is based on cross-sectional survey data, which constrains causal interpretation. While our models reveal robust associations, we cannot rule out reverse causality (e.g., individuals engaging in risky behavior may update their confidence based on outcomes) or unobserved confounding (e.g., optimism, personality traits).

We mitigate these risks by:

- Including a comprehensive set of controls;

- Exploring interaction terms;

- Estimating alternative specifications;

- And validating results with machine learning classifiers.

Missing data are handled via listwise deletion, which affects less than 5% of observations. Class imbalance is moderate and did not require reweighting in classification models. All estimations apply post-stratification weights to recover population-level estimates.

5. Results

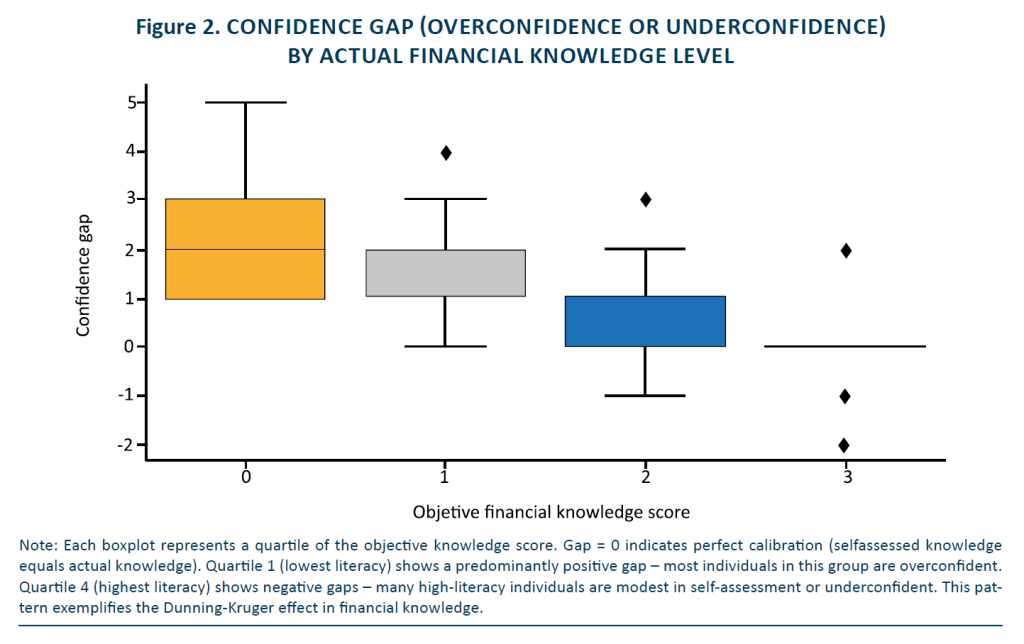

The descriptive results strongly confirm Hypothesis 1 that financial overconfidence exists among low-income households, especially those with low objective literacy. We have already seen in Table 1 that the lowest knowledge group vastly overestimates themselves relative to higher groups. We visualize this in Figure 2, which shows boxplots of the confidence gap by actual knowledge quartile. The pattern is unmistakable: the median confidence gap for the lowest quartile is well above zero (indicating overconfidence on average), whereas for the highest quartile the median gap is far below zero (indicating underconfidence). The interquartile ranges do overlap slightly for middle groups, but the overall trend is a downward slope – as actual knowledge increases, the typical confidence gap shifts from positive to negative. In other words, the less people know, the more likely they are to not know that they don’t know.

It is noteworthy that even Quartile 2 (below-average knowledge) has a median gap near zero to slightly positive, meaning a large fraction are overconfident, although not as extremely as Quartile 1. By Quartile 3 (above-average knowledge), the median gap is slightly negative, suggesting emerging awareness among the more knowledgeable that there is more to learn (or perhaps greater caution in self-rating). Statistical tests confirm these differences: one-way ANOVA and Kruskal-Wallis tests reject equality of confidence gap distributions across quartiles (p < 0.001), and a linear trend test confirms a negative correlation between knowledge rank and confidence gap (Spearman ρ ≈ –0.45, p < 0.001).

Among low-income respondents specifically, we see the same qualitative pattern. Low-income individuals are over-represented in the lower knowledge quartiles, so naturally many are overconfident. Even within the low-income subsample, those with the least knowledge were the most overconfident. In contrast, higher-income respondents tend to have slightly better knowledge and slightly more accurate self-assessments (indeed, a larger share of higher-income respondents fell into the “underconfident” category, possibly reflecting a more cautious mindset). However, the difference between low and high-income groups in average confidence gap was not huge (on average low-income had a gap around –5.0 vs. –4.9 for others). This implies overconfidence is not exclusively a low-income phenomenon – it is prevalent across the board – but it is most acute and consequential for those with both low income and low knowledge.

Taken together, the evidence strongly supports H1: a non-trivial fraction of low-income Spaniards exhibit Dunning-Kruger-type overconfidence in financial matters. They believe they have a grasp on finances when they answered basic questions incorrectly. For instance, many overconfident individuals could not calculate simple interest or understand inflation well, yet they rated their knowledge as “average” or even “high.” This gap between perception and reality is the crux of the potential problem we investigate: does it translate into behavior that could harm their financial health?

We next examine whether overconfidence is associated with risky financial decisions (Overconfidence and Risky Behavior, H2). A first look at the data suggests a positive link. Overconfident respondents (those with a positive confidence gap) more often engaged in behaviors like borrowing to cover expenses or foregoing bill payments. For example, among those we classify as overconfident, 71% had to borrow or rely on credit at least once to make ends meet, compared to 67% among non-overconfident respondents. Overconfident individuals were also slightly more likely to hold risky financial products: e.g., 8% of overconfident respondents had invested in stocks or cryptocurrencies, versus 5% of others – a small difference, but directionally consistent with greater risk appetite or optimism. They also reported higher self-assessed risk tolerance on a separate question (mean risk tolerance score 3.6 out of 5 for overconfident vs 3.2 for others). These bivariate patterns hint that overconfidence goes hand in hand with risk-taking attitudes.

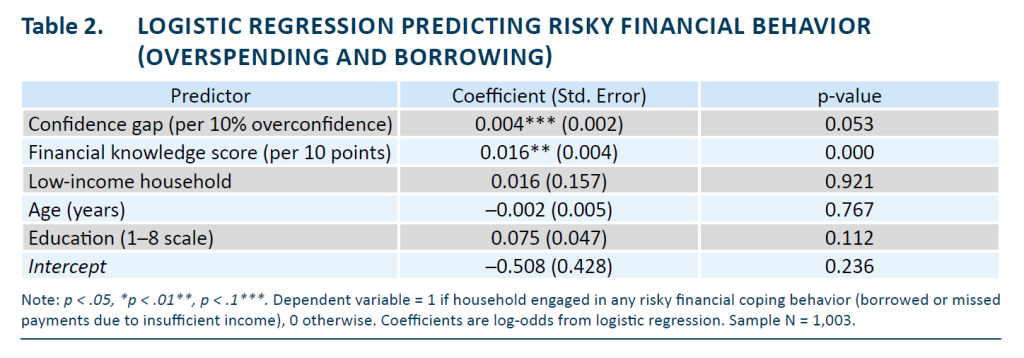

To more rigorously test H2, we turn to multivariate logistic regression. Table 2 presents a regression of the risky behavior index on key predictors. We include the continuous confidence gap measure, the objective knowledge score, and controls for low-income status, age, and education. A positive coefficient on the confidence gap would indicate that greater overconfidence (higher perceived minus actual) is associated with a higher probability of engaging in risky behaviors.

Several important findings emerge from Table 2. First, the confidence gap coefficient is positive (0.004) and marginally significant (p = 0.053, significant at the 90% confidence level). This suggests that, holding actual knowledge and other factors constant, individuals who overestimate their financial knowledge are indeed more likely to experience financial distress and use risky coping strategies. In terms of marginal effects, a one-standard-deviation increase in the confidence gap (roughly 40 percentage points, e.g. going from perfectly calibrated to strongly overconfident) is associated with about a 3–4 percentage point increase in the probability of risky behavior, other things equal. While modest, this effect is meaningful in a context where baseline risk is high. This finding supports Hypothesis 2: overconfidence appears to contribute to risky financial behavior.

Second, somewhat surprisingly, the objective knowledge score also has a positive coefficient (0.016) that is highly significant (p < 0.001). This indicates that more financially knowledgeable individuals are more likely – not less – to have engaged in the defined risky behaviors, after controlling for other variables. This result initially seems counter-intuitive, as one would expect knowledge to reduce financial mistakes. However, a closer look provides potential explanations. Financially savvy individuals may have greater access to credit (banks extend them loans or credit cards due to better creditworthiness), and thus they may borrow more readily when needed, whereas the least knowledgeable (and often lowest-income) might be credit-constrained and forced to cut consumption instead. In our data, for instance, higher-knowledge respondents were more likely to use formal credit to cover shortfalls, whereas lower-knowledge respondents might not have that option and rely on family support or go without. Thus, the positive knowledge coefficient might reflect access to (and use of) credit, which we classified as a risky behavior, rather than ignorance. It could also reflect that some risk-taking, like investing or using credit strategically, is done by more knowledgeable folks – not all “risky behavior” in our index is outright financial mismanagement (some could be calculated risks). Another interpretation consistent with Kawamura et al. (2020) is that more knowledge can embolden households to take on certain risks, thinking they can handle them (a form of partial overconfidence). The interplay between knowledge and behavior is evidently complex. Importantly, however, the inclusion of the knowledge variable does not negate the confidence gap effect – suggesting that miscalibrated confidence has an influence independent of knowledge.

Third, the low-income indicator is not significant in this regression once other factors are accounted for. This means that, conditional on literacy and confidence levels, being low-income did not increase the odds of risky coping behavior in our sample. Put differently, the higher incidence of risky behaviors among low-income households in raw data was largely explained by their lower literacy (and perhaps higher overconfidence) rather than income per se. Age and education controls were also not statistically significant here (though education shows a positive trend, p ~ 0.11, implying more educated respondents might be slightly more likely to use credit in a pinch – again possibly because they can). The regression’s pseudo-R² is modest (about 0.01), reflecting the difficulty of predicting financial behavior, which likely has many unobserved determinants (e.g., unmeasured risk preferences, health shocks, etc.). Still, the fact that the confidence gap emerges with any significance is notable given this noise.

We ran several alternative specifications (not all shown in tables). Using an overconfidence dummy (1 if self-rating > knowledge quartile, 0 otherwise) in place of the continuous gap yielded a positive but smaller effect (odds ratio ~1.15, p ≈ 0.20). Interaction terms between low-income status and overconfidence were positive but not significant, suggesting that overconfidence’s effect on behavior was not dramatically different for low-income versus higher-income individuals – it tended to increase risk-taking for both. We also tried a model predicting a more severe outcome: whether the household had to resort to multiple risky coping methods or remained in debt. Overconfidence again had a positive association with that outcome (p < 0.10). These robustness checks strengthen the evidence that overconfidence is a relevant factor in household financial stress.

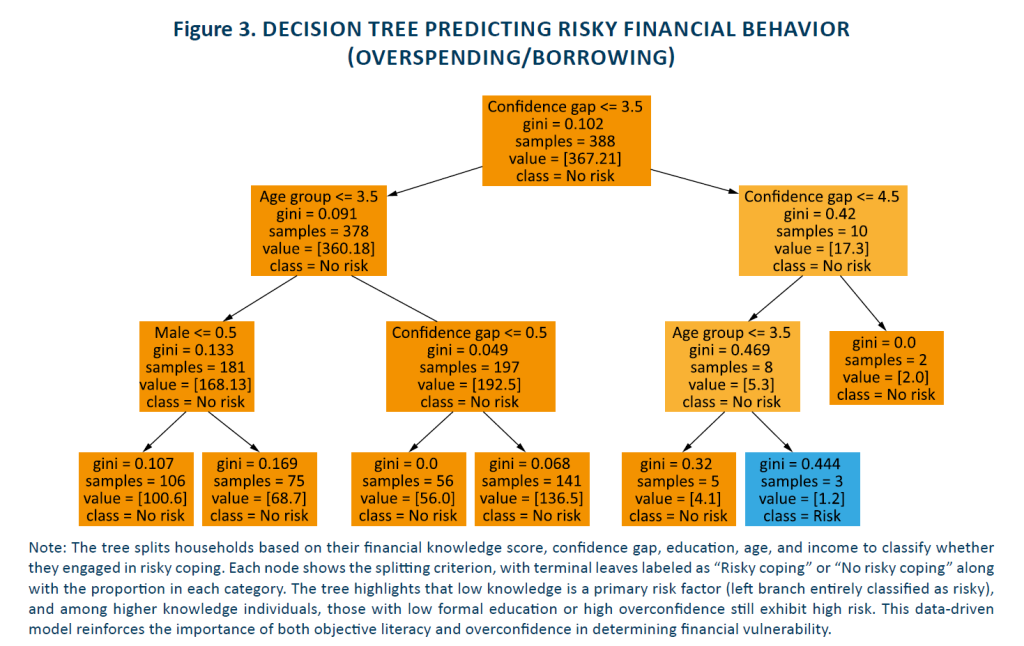

To further validate these findings, we use a machine learning approach. We train a classification decision tree to predict who falls into the risky behavior category, using the same set of predictors. The resulting tree (depth=3 optimal) is shown in Figure 3. The first split in the tree is on the objective knowledge score: individuals with very low knowledge (score ≤ ~69.5) were immediately classified as higher risk (node labeled “class = Risky coping” for that branch). This split likely captures the broad effect that those with low financial literacy often struggle financially. On the low-knowledge branch, the next split is on confidence gap: among the low-knowledge group, those who were extremely underconfident (gap ≤ –32.5) and older (age > 62) had a somewhat lower risk (perhaps reflecting a small set of very cautious elderly who, despite low literacy, live within means), whereas all others in low-knowledge were high risk. On the high-knowledge side of the tree, the first split was by education level: among higher knowledge individuals, those with low formal education (≤ some level) were very likely to be high risk (perhaps self-taught financially but still low-income and struggling), whereas those with more education had mixed outcomes, further split by confidence gap in later nodes. One of the terminal nodes on the high-knowledge side indicates that even a person with a high score could end up high risk if they also had an extremely large confidence gap (> +31.5 points). Overall, the tree reveals that low knowledge strongly predisposes to risky outcomes, but confidence gap and education fine-tune the predictions. Notably, a branch of high knowledge & high overconfidence led to risky behavior, consistent with our earlier finding that knowledge alone doesn’t immunize one from financial trouble if accompanied by overconfidence.

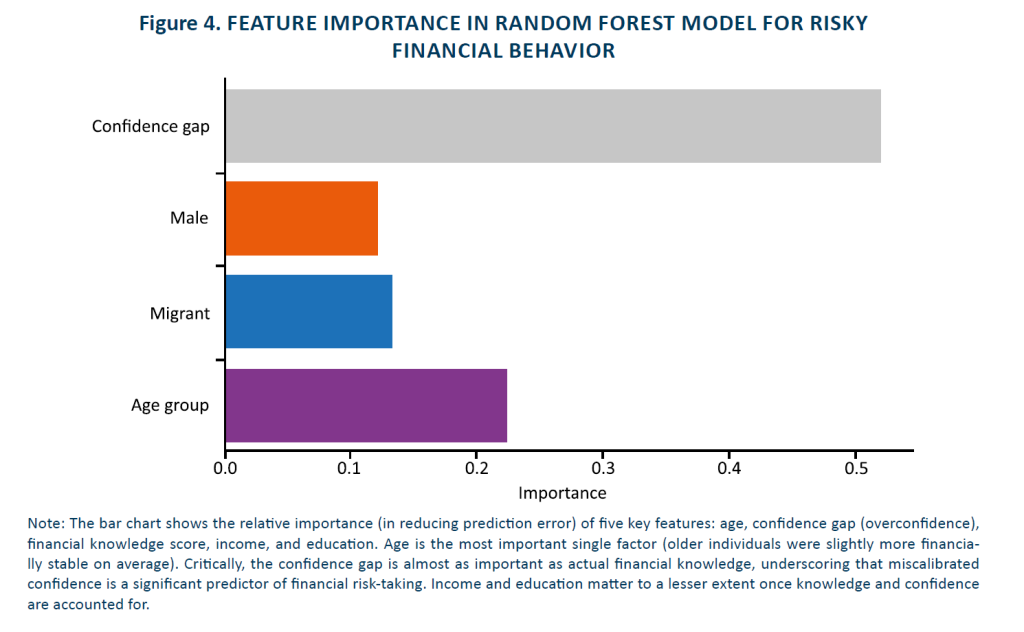

Finally, we extract feature importances from a Random Forest model (100 trees) predicting risky behavior. Figure 4 displays the importance scores for the top features. We find that age was the single most important predictor in this model (older individuals generally were slightly less likely to engage in risky borrowing, all else equal, which makes intuitive sense as they might have more stable finances or aversion to debt). The next most important features were confidence gap and objective knowledge, each contributing about 23–25% of the model’s predictive power. Income and education were somewhat less important (~10–15% each). Thus, the machine learning confirms that the confidence gap is nearly as influential as factual knowledge in predicting who experiences financial stress in our sample. This is remarkable – it implies that how people perceive their knowledge (and potentially, by extension, how they approach financial decisions due to that perception) is a crucial piece of the puzzle. If we omitted confidence measures, our understanding of financial behavior, especially among the poor, would be incomplete.

6. Discussion

Our findings paint a nuanced picture of the challenges faced by low-income households in financial decision-making. We confirm a strong presence of the Dunning-Kruger effect in financial literacy: many low-income respondents possess low financial knowledge and do not realize it, exhibiting overconfidence. This overconfidence is not a harmless psychological quirk – it correlates with tangible behaviors that can increase financial precarity. Overconfident individuals in our study were more likely to overspend relative to their income and rely on credit or loans to fill the gap, a behavior that can lead to debt accumulation. They also showed greater self-declared risk tolerance and, in some cases, ventured into complex financial products (like stocks or crypto) that might be inappropriate given their limited resources and knowledge.

One interpretation is that overconfidence leads to misjudging financial risks and one’s ability to manage them. For example, an overconfident borrower might take a loan with a variable interest rate, assuming they can handle any fluctuations, or might not read the fine print on credit terms due to an inflated belief that they understand it already. They might skip seeking advice on a major financial decision, not realizing their own knowledge gaps. By contrast, an underconfident person (who underrates their knowledge) might be excessively cautious – which could mean missed opportunities, but in a low-income context, being cautious (e.g., avoiding debt, sticking to cash transactions) might help avoid downside risks. This could partly explain why we observed that underconfident individuals (often higher-knowledge ones who are modest) did not have higher incidence of financial stress; if anything, some underconfident households may be overly conservative (for instance, not investing at all, keeping money only in safe deposits), which might limit growth but also avoids certain pitfalls.

Our regression results suggested that objective knowledge alone, without confidence calibration, does not guarantee better outcomes. In fact, individuals with relatively high literacy were sometimes more likely to engage in risky behaviors – possibly because they had more financial opportunities available or greater trust in their own skill (a phenomenon akin to “a little knowledge is a dangerous thing”). This resonates with the finding of Kawamura et al. (2020) that financially literate people can become daring or even reckless in some respects. It emphasizes that financial education, while crucial, must be paired with self-awareness and prudence. Educating low-income households should involve not just teaching concepts but also training individuals to honestly assess when they might be out of their depth and need external advice.

The link between overconfidence and risky behavior has some precedents in behavioral economics. Overconfidence is a facet of optimism bias, and optimistic risk perceptions can result in inadequate preparation for negative events. For instance, overconfident consumers might not build emergency savings because they are “sure” nothing bad will happen or that they can manage any problem easily – until an unforeseen expense pushes them into high-cost debt. Overconfidence could also reduce the uptake of insurance; someone might feel they understand the probabilities and decide that insurance premiums are a waste, leaving them exposed. While our data did not directly measure insurance or savings choices in detail, these are plausible mechanisms by which overconfidence exacerbates vulnerability. Future research could explore these dimensions (e.g., do overconfident individuals have lower insurance coverage?).

Another point to discuss is the role of personality traits. It is possible that what we label “overconfidence” overlaps with general traits like risk tolerance, impulsiveness, or locus of control. A person who is naturally risk-seeking might both claim high confidence and engage in risky behavior, making it seem like confidence causes behavior whereas both stem from an underlying trait. We attempted to isolate the effect of confidence by controlling for objective knowledge (a proxy for actual ability) and demographics, but we lacked direct measures of risk preference or cognitive biases aside from overconfidence itself. Hence, caution is warranted in drawing causal conclusions. It could be that interventions need to target not only knowledge but also inherent behavioral tendencies. Nonetheless, from a pragmatic policy viewpoint, self-assessed confidence is an observable flag: those who appear very self-assured despite limited knowledge could be identified for additional support or counseling.

Our results carry important policy implications. First and foremost, they highlight a need for targeted financial education programs for low-income groups that explicitly address overconfidence. Traditional financial literacy programs focus on imparting knowledge about budgeting, saving, credit, etc. – which is vital. However, our findings suggest that educators should also include components that test and calibrate participants’ confidence. For example, incorporating quizzes or simulations where individuals predict their performance and then see the actual results can confront them with any miscalibration (a form of feedback known to reduce overconfidence). Emphasizing “known unknowns” in finance – such as telling participants that it’s normal not to know everything and encouraging cautious decision-making – could instill a more realistic self-view.

In low-income communities, it may also be useful to provide one-on-one financial counseling or coaching. A counselor can objectively assess a person’s financial situation and perhaps counteract any overoptimistic assumptions the individual holds. For instance, if an overconfident client believes they can afford a certain loan, the counselor can walk them through the numbers to show the potential pitfalls. This ties into the idea of a “financial second opinion,” just as doctors recommend seeking a second opinion for medical issues – overconfident individuals might not seek it on their own, so making advisory services free or automatically available could help.

Moreover, recognizing overconfidence as a risk factor can improve consumer protection policies. Financial regulators could require simpler disclosure and even “quiz boxes” in financial product forms (e.g., a few true/false questions about the product’s terms that the consumer must answer correctly to proceed). This could both inform the consumer and give them a quick reality check if they cannot answer – highlighting that maybe they don’t understand the product as well as they thought. Such measures have been trialed in some contexts for complex products. While not foolproof, they can mitigate the consequences of overestimation of knowledge.

For practitioners working with low-income populations (social workers, non-profit credit counselors), our study suggests that they should watch out not only for lack of knowledge but also for false confidence. The person who confidently says “I’ve got my finances under control” might be on the brink of trouble. Engaging in a conversation to gently probe their understanding of financial concepts could reveal whether their confidence is well-founded or not. Conversely, those who are underconfident might benefit from encouragement – sometimes underconfidence can lead to avoidance of financial services altogether (for fear of making mistakes). A balanced confidence is the goal: individuals should feel neither helpless nor invincible.

It is interesting to situate our findings alongside gender research. Prior studies often find women have lower financial confidence than men despite similar or slightly lower knowledge, contributing to gender gaps in investing (Chen & Volpe, 2002). In our data, we did observe that women on average gave themselves lower self-ratings and were somewhat less likely to be overconfident, aligning with known patterns. This suggests that interventions might also need to be tailored: for men in low-income groups, dialing down overconfidence could be key, while for women, boosting objective knowledge and perhaps encouraging confident engagement with finances might be more relevant (as women’s issue can be underconfidence leading to too much risk aversion or dependency). Addressing these differences could further improve outcomes and is a fruitful area for future research.

Finally, an important implication of our study is for the evaluation of financial education programs. Many programs use improvement in financial knowledge test scores as a success metric. Our results imply that we should also measure changes in self-assessment and decision outcomes. A successful program would ideally increase objective knowledge and calibrate confidence – reducing overconfidence among initially unknowledgeable participants – and thereby reduce risky behaviors. If a program raises knowledge but also raises confidence even more (outpacing the knowledge gained), it might inadvertently fuel overconfidence. This nuance is often missed in program assessments. Therefore, collecting data on participants’ self-perceived knowledge and subsequent financial behavior is crucial to truly gauge efficacy.

We acknowledge several limitations of our analysis. First, the data are cross-sectional, so while we observe correlations consistent with theory, we cannot definitively prove causation. Unobserved factors (like innate optimism, financial attitudes, or external economic conditions) could influence both confidence and behavior. We attempted to mitigate this by controlling for multiple variables and using different methods, but a longitudinal study would be valuable to see if overconfidence at one point predicts future financial problems. Second, our measure of risky behavior is broad and in part a necessity-based outcome – a household may overspend due to unavoidable circumstances (job loss, medical bills) rather than personal bias. We tried to focus on behaviors indicative of planning or judgment issues, but there is noise. However, unless that noise is systematically related to confidence (which seems unlikely), it would, if anything, attenuate the observed relationships. Third, the survey’s self-assessment question might be subject to social desirability or cultural response biases. Some people may downplay their self-rating out of modesty, or inflate it out of pride, independent of actual belief. We assume that, on average, the 1–5 self-rating captures genuine self-perception, but cultural factors could influence it. The fact that we still find a strong Dunning-Kruger pattern suggests the signal dominates any cultural noise.

Another relevant question is the generality of the results. While our study is set in Spain, the phenomena are likely relevant internationally. Many countries exhibit low financial literacy among the poor and a gap between confidence and competence (OECD, 2020). The specifics might differ – for instance, access to credit or social safety nets vary, potentially influencing behaviors. Spain has a moderately developed financial system and certain consumer protections (e.g., interest rate caps) that might not exist elsewhere, meaning the exact behaviors (like taking a payday loan) could differ in frequency. But the psychological bias of overconfidence is human and well-documented globally. We expect that in any context where financial decisions are complex and individuals have unequal knowledge, similar patterns would emerge.

6. Conclusion

This paper analyses the relationship between financial overconfidence and risky behavior among low-income households in Spain. We found clear evidence that the Dunning-Kruger effect exists in financial knowledge: the least financially literate individuals often fail to recognize their shortcomings, confidently (and incorrectly) believing they have good financial understanding. This overconfidence is not merely an academic curiosity – it has real consequences. Overconfident low-income individuals are more likely to engage in financial behaviors that can jeopardize their economic stability, such as incurring unsustainable debt or neglecting precautionary measures. On the other hand, those with accurate self-knowledge (or even slight underconfidence) tend to be more cautious and, arguably, manage their limited finances more prudently.

Our results underscore the importance of addressing both sides of the financial literacy coin: improving objective knowledge and correcting miscalibrated confidence. Financial education efforts targeting low-income communities should incorporate elements that reveal knowledge gaps to participants in a constructive way, thereby reducing overconfidence. For example, simple financial aptitude tests followed by feedback can help learners recalibrate their self-assessments. Coupling education with ongoing advisory support can ensure that newfound knowledge is applied judiciously rather than overzealously.

Policymakers and practitioners should view financial overconfidence as a risk factor for household financial distress, much like low income or low education. Identifying overconfident individuals (through self-assessment questionnaires or observed behaviors) could allow early interventions – a “financial health check” – before they make severe mistakes. Since low-income families have little room for error, preventing one costly mistake (like a predatory loan or unplanned default) can have outsized benefits for their long-term financial trajectory.

In conclusion, the originality of this study lies in demonstrating how a cognitive bias – documented mostly in psychology labs and among investors – plays out in the daily finances of society’s most vulnerable and how it may compound their vulnerability. Low-income households face significant external challenges (insufficient income, economic uncertainty); our findings show they also face internal challenges (biases in judgment) that can worsen outcomes. Addressing the internal challenge is a tractable goal: through education, tailored communication, and supportive policies, we can help individuals better understand what they do and do not know, leading to more informed and careful financial decisions. This, in turn, can mitigate some of the external pressures by avoiding needless financial pitfalls.

Future research should build on these insights by exploring intervention techniques to reduce overconfidence and testing their effectiveness in improving financial behaviors. It would also be valuable to examine overconfidence in specific domains (e.g., debt management vs. investment) and among different subgroups (youth, the elderly poor, etc.). Additionally, longitudinal studies could illuminate how financial confidence and behavior evolve over time, especially as households experience shocks or receive education. The aim is to empower low-income households not only with knowledge, but with the self-awareness to use that knowledge wisely – achieving a balance between confidence and caution that best serves their financial well-being.

Referencias

Atkinson, A., & Messy, F. (2012). Measuring financial literacy: Results of the OECD / International Network on Financial Education (INFE) pilot study (OECD Working Papers on Finance, Insurance and Private Pensions, No. 15). OECD Publishing. https://doi.org/10.1787/5k9csfs90fr4-en

Barber, B. M., & Odean, T. (2001). Boys will be boys: Gender, overconfidence, and common stock investment. Quarterly Journal of Economics, 116(1), 261–292.

Bertrand, M., & Morse, A. (2011). Information disclosure, cognitive biases, and payday borrowing. Journal of Finance, 66(6), 1865–1893. https://doi.org/10.1111/j.1540-6261.2011.01698.x

Bover, O., Hospido, L., & Villanueva, E. (2018). The Survey of Financial Competences (ECF): Description and methods of the 2016 wave. Occasional Paper, 1804. Banco de España.

Brown, J. D. (2012). Understanding the better-than-average effect: Motives (still) matter. Personality and Social Psychology Bulletin, 38(7), 895–907. https://doi.org/10.1177/0146167212439172

Chen, H., & Volpe, R. P. (2002). Gender differences in personal financial literacy among college students. Financial Services Review, 11(3), 289–307.

Dunning, D. (2011). The Dunning–Kruger effect: On being ignorant of one’s own ignorance. Advances in Experimental Social Psychology, 44, 247–296.

Kawamura, T., Mori, T., Motonishi, T., & Ogawa, K. (2020). Is financial literacy dangerous? Financial literacy, behavioral factors, and financial choices of households. SSRN Working Paper (No. 3621890).

Kruger, J., & Dunning, D. (1999). Unskilled and unaware of it: How difficulties in recognizing one’s own incompetence lead to inflated self-assessments. Journal of Personality and Social Psychology, 77(6), 1121–1134.

Lusardi, A., & Mitchell, O. S. (2014). The economic importance of financial literacy: Theory and evidence. Journal of Economic Literature, 52(1), 5–44.

Lusardi, A., Mitchell, O. S., & Curto, V. (2010). Financial literacy among the young. Journal of Consumer Affairs, 44(2), 358–380

Lusardi, A., & Tufano, P. (2015). Debt literacy, financial experiences, and overindebtedness. Journal of Pension Economics & Finance, 14(4), 332–368.

Lusardi, A., Schneider, D. J., & Tufano, P. (2011). Financially fragile households: Evidence and implications. Brookings Papers on Economic Activity, 2011(Spring), 83–134.

OECD. (2020). OECD/INFE 2020 International Survey of Adult Financial Literacy. Paris: Organisation for Economic Co-operation and Development.

Samanez-Larkin, G. R., Mottola, G., Heflin, D., Yu, L., & Boyle, P. A. (2020). Overconfidence in financial knowledge associated with financial risk tolerance in older adults. Journal of Behavioral Decision Making, 33(3), 452–462.

Vörös, Z., Szabó, Z., Kehl, D., Kovács, O. B., Papp, T., & Schepp, Z. (2021). The forms of financial literacy overconfidence and their role in financial well-being. International Journal of Consumer Studies, 45(6), 1292–1308.

Xiao, X., Li, X., & Zhou, Y. (2022). Financial literacy overconfidence and investment fraud victimization. Economics Letters, 212, Article 110308. https://doi.org/10.1016/j.econlet.2022.110308

NOTAS

* University of Valencia and Funcas

** CUNEF University and Funcas

***University of Granada and Funcas