The interdependencies of Canadian financial institutions: An application to climate transition shocks

Climate change, financial stability, financial institutions, financial markets, economic models

Gabriel Bruneau, Javier Ojea-Ferreiro, Andrew Plummer, Marie-Christine Tremblay and Aidan Witts*

Papeles de Energía, N.º 26 (septiembre 2024)

We develop a methodological framework, combining scenario analysis and agent-based model, that captures the direct effects of a stressful climate transition shock as well as the indirect –or systemic– implications of these direct effects. We apply this framework using data from the Canadian financial system. To capture the direct effects, we leverage the climate transition scenarios and financial risk assessment methods developed for the Bank of Canada and the Office of the Superintendent of Financial Institutions climate scenario analysis pilot project. We examine the direct effects –in the form of credit, market and liquidity risks– of the climate transition shock on financial system entities within the scope of our study. Specifically, we look at the public and private assets and derivatives portfolios of deposit-taking institutions, life insurance companies, pension funds and investment funds. To assess the indirect effects from the potential spread of the climate transition shock across an interconnected financial system, we extend an agent-based model to explore shock transmission channels such as cross-holding positions, business similarities, common exposures and fire sales. This model considers rules and behavioural assumptions, allowing us to understand the interconnectedness of the financial system. This work strengthens our understanding of how distinct entities within the financial system could be impacted by and respond to climate transition risks and opportunities, and of the potential channels through which those risks and opportunities may spread. More generally, this work contributes to building standardized systemic risk assessment and monitoring tools.

1. INTRODUCTION◆

The financial system is inherently vulnerable to systemic risks, due to factors such as interconnectedness, agency problems causing asymmetric information, and feedback mechanisms like fire sales and herd behavior. To prevent system-wide breakdown, regulatory authorities prioritize building a resilient financial sector. Analytical tools that identify shocks and risk sources are crucial in this endeavor. By assessing how individual issues could propagate during period of financial stress, policymakers can proactively adjust prudential instruments to ensure stability.

This paper introduces a model that captures system-wide amplifications of shocks to market, credit, and liquidity risks across various financial sectors and entities. The model describes shock propagation from a system-wide perspective in a financial network comprising deposit-taking institutions, life insurance companies, investment funds, and pension funds. Each participant’s role in the model can either exacerbate or mitigate the direct effects of shocks, depending on their business model, exposure to shocks, and interconnections with other market participants. Our framework’s contagion process accounts for credit deterioration and varying fire sale sensitivities based on asset types. It also incorporates intersectoral lending, cross-holding effects through equities and funds’ participations, and the liquidity effects of derivatives. We apply our model to assess the Canadian financial system’s response to a delayed 2 ºC climate transition scenario.

Our research makes contributions to the field of financial stability and systemic risk in several ways. We build upon Hałaj’s (2018) model and analysis by incorporating life insurance companies and pension funds and examining the role of margin calls. We explore how derivatives and credit deterioration can trigger to liquidity issues, exacerbating overall liquidity conditions through intersectoral lending channels. To our knowledge, no prior study has investigated the role of derivatives, intersectoral lending linkages, and credit deterioration in the pension fund sector. While other researchers like Cont et al. (2020) have analyzed the linkages between liquidity and solvency in the banking sector, these aspects are not considered in Hałaj’s (2020) application of his 2018 framework using Canadian data. Furthermore, we assess fire sales contagion by examining the impacts of sales pressure on asset prices and computing sensitivities based on quantile regression (see Fukker et al., 2022).

We also trace contagion between institutions, building contagion indicators based on network analysis (see Bardoscia et al., 2021). Our investigation delves into the role of pension funds within in the financial system, a topic that has not been extensively explored in the literature. For instance, Douglas and Roberts-Sklar (2018) examine the behavior of defined benefit pension funds in the UK, while Bédard-Pagé et al. (2021) describe the behavior of Canadian pension funds during the COVID crisis. Our study addresses these potential liquidity issues into account and incorporates insights from discussions with Canadian pension funds’ asset managers, focusing on climate transition.

Additionally, we contribute to the literature on the effects of climate transition on the financial system by applying our methodological framework to assess the spread of climate transition risk in the Canadian financial system. This analysis leverages climate transition risks scenarios from the Bank of Canada-Office of the Superintendent of Financial Institutions (OSFI) pilot project, supervisory data from the Office of the Superintendent of Financial Institutions (OSFI) and l’Autorité des Marchés Financiers(AMF), third-party data from LSEG Lipper, and bilateral agreements with several pension funds and asset managers of pension funds. Notably, this is the first system-wide climate transition risk analysis using Canadian data. Previous studies, such as Roncoroni et al. (2021), have used Mexican financial system data to analyze climate transition transmission within banking and investment funds sectors, while others like Gourdel and Sydow (2023) and Battiston et al. (2017) have focused on the EU financial system.

Our findings illustrate how a delayed climate transition scenario transmits through the Canadian financial system, revealing modest direct impacts. This partly reflects the limited exposure of Canadian financial entities to sectors negatively impacted by the transition, as well as the exposure of some financial entities to sectors positively impacted by the transition. However, the interconnections identified in our study play a significant role in spreading the impacts of climate transition risk. Key transmission channels include common exposures, fire sales, and cross-holding positions. Investment funds are the primary contributors to shock propagation due to their procyclical behavior and susceptibility to redemption shocks. In contrast, pension funds, with their long-term investment horizons and stable contributor base, may mitigate contagion effects by capitalizing on undervalued assets.

The rest of the paper is structured as follows. In Section 2, we present the model. Section 3 outline the datasets employed to conduct the analysis, and present the results, and Section 4 draws conclusions.

2. Methodological framework to assess systemic risks

The methodological framework we develop combines two analytical tools. We use scenario analysis to capture the direct effects of climate transition shocks on individual financial entities, and we use agent-based modelling to examine the indirect, or systemic, effects of these shocks. We describe both of these methods below.

Although the shock modeled in this analysis is a climate transition risk, our agent-based model is general enough to be initialized by other types of macroeconomic and/or financial shocks, to study a wide range of systemic risk.

2.1. Examining direct effects on financial system entities through scenario analysis

Because of its forward-looking nature and inherent uncertainty about future events, climate transition risk is difficult to assess using standard methodologies that rely on historical data. This difficulty is compounded by further uncertainty about how policy, technology and socioeconomic factors might evolve. In this context, scenario analysis serves as a flexible “what if” tool that is useful for exploring potential risks and opportunities under various possible futures. The scenarios are neither forecasts nor intended to be comprehensive but instead serve as plausible pathways designed to achieve specific climate targets.1

2.1.1. Leveraging the Bank of Canada’s climate transition scenarios

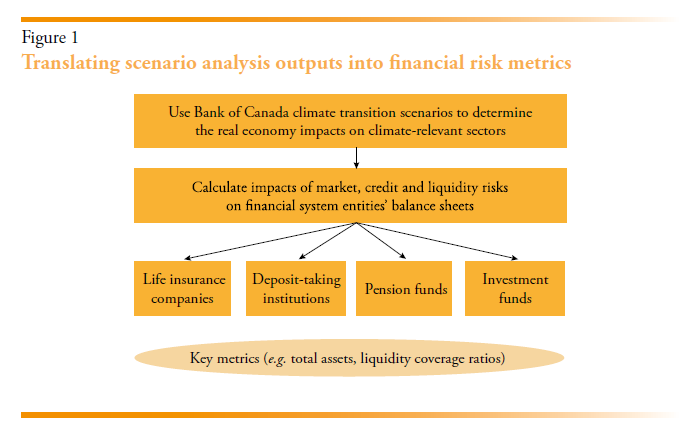

Figure 1 shows the steps taken to capture the direct effects of a climate transition shock on distinct types of financial system entities through scenario analysis.

We leverage the set of global climate transition scenarios developed for the Bank of Canada and OSFI climate scenario analysis pilot project. The scenarios cover many geographical regions of the world. The scenarios were intentionally designed to be adverse but plausible, capturing situations that have the potential to be stressful to the Canadian economy and the financial system. These are the two climate transition scenarios we leveraged in this analysis:2

- baseline (2019 policies)–a baseline scenario consistent with global climate policies in place at the end of 2019

- below 2 °C delayed–a delayed policy action toward limiting average global warming to below 2 °C, which is the most severe climate transition scenarios analyzed by the Bank of Canada in its pilot project.

We also adopt the pilot project’s climate-relevant sectors. These are sectors that are likely to be most affected, either negatively or positively, by the transition pathways. Some broad sectors, such as oil and gas, electricity, energy-intensive industries, and commercial transportation, were broken down into smaller groups because the transition may play out differently for those sub-sectors.3 This provided sectoral groupings that are largely homogeneous in terms of climate transition exposures.

The scenarios were then used to define sectoral risk factor pathways (RFPs), reflecting changes in four components affecting a sector’s net income that may be impacted by the transition: direct emissions costs, indirect costs, capital expenditures and revenues.4 The cumulative effect of changes in these different components illustrates how a sector can be affected by the transition, including the financial distress that it may encounter.5

2.1.2. Translating scenario outputs into financial risk metrics

We also leverage the pilot project’s risk assessment methods to translate the scenario outputs into measures of credit and market risk. In the pilot project, the credit risk assessment method combined top-down and bottom-up assessments. A borrower-level impact assessment exercise using the scenarios’ sectoral financial impacts (the RFPs discussed above) was conducted in the pilot project’s bottom-up assessment. In the top-down assessment, the impacts from the bottom-up assessment were extrapolated to portfolio segments with similar transition risk exposures. Leveraging these assessments, the pilot project estimated a climate transition–credit risk relationship using a Merton-style model. For each sector-region pair, the model mapped scenario RFPs and heat map sensitivities into changes in probability of default. Then a Frye–Jacobs relationship was used to assess loss given default based on the probabilities of default. Finally, the credit risk was assessed through expected credit losses, which was based on projected probabilities of default, loss given default and exposures at default.6

The market risk assessment method used a top-down approach. Climate transition scenario impacts on equity valuations for each sector-region pair were determined based on a discounted dividend model.7 Sectoral dividends were calculated from projected income along the transition paths, considering a given capital share of value added and a dividend rate. Also, for tractability, global climate policy commitments were assumed to be upheld and incorporated into equity valuations immediately at the time of the policy announcement, implying a discrete change in valuations at the time of the policy change. Economic agents were assumed to have foresight over a 10 year rolling window of climate policy, with the policy remaining constant from that point on. This implies a gradual adjustment in equity valuations following the discrete jump driven by the change in global policy climate pathways.8

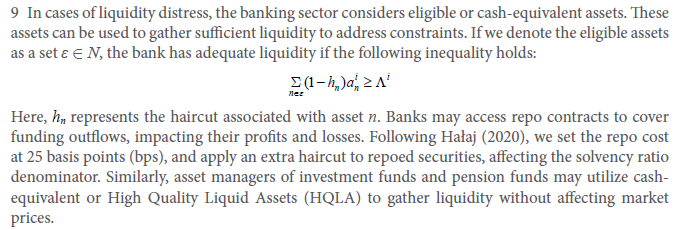

Including liquidity risk is key in understanding systemic risk. The liquidity risk assessment method is another extension of the pilot project’s methods. Consistent with the goals of this study, the inclusion of a liquidity risk channel can inform us of the difficulties entities may face in meeting their short-term financial obligations. This could be due to an inability to convert their assets into cash without incurring a substantial loss. Specifically, we examine the liquidity held by financial system entities before the climate transition shock and their liquidity needs after the shock.9

The liquidity held by a given entity is determined by weighting its asset positions by a Basel III-based liquidity factor.10 We calculate liquidity measures for deposit-taking institutions, open-ended mutual funds (for investment fund entities) and pension funds. We assume that the cash flow on the liquidity coverage ratio framework for deposit-taking institutions follows the run-off rate from OSFI and the Autorité des Marchés Financiers (AMF) net cumulative cash flow returns. For open-ended mutual funds, we use historical data to estimate the expected cash outflows through redemptions. Finally, while pension funds have predictable outflows to pay their beneficiaries, they face relatively less-predictable liquidity constraints from their derivative positions.11 Because of this, increased liquidity needs for derivatives positions are captured by a volatility-based measure (Standard Portfolio Analysis of Risk, or SPAN) for equity-related derivatives and a Monte Carlo simulation for debt-related derivatives.

In our model, institutions face market, credit, and liquidity shocks. Market shocks reduce asset values and equity, impacting solvency ratios. If an asset suffering a market loss has a positive liquidity weight ratio, it can also affect liquidity ratios. Credit shocks, driven by default risk, further impact solvency ratios through the decrease of equity and a potential increase of risk weighted assets. Additionally, credit deterioration may render an asset no longer high-quality, affecting liquidity ratios. Finally, liquidity shocks–such as redemption shocks–can decrease the liquidity ratio.

Finally, as shown in Figure 1, our analysis centers on two types of key metrics for assessing market participants’ actions: solvency ratio and liquidity ratio. Pension funds and investment funds prioritize liquidity ratio, while life insurance companies focus on solvency ratio. The banking sector takes both liquidity and solvency ratios into account.12

2.2. Examining systemic effects using agent-based modelling

Agent-based modelling is a computational approach in which heterogeneous agents interact in accordance with given decision rules (e.g., behavioural, regulatory) and where the spread of the shock depends on the linkages across the agents in the system. Agent-based models (ABMs) can thereby provide rich analytical insights about the systemic implications of a given shock. Indeed, both entity-specific details (like risk profiles and portfolio characteristics) and commonalities and financial linkages across entities are core features of the financial system that can be modelled through an ABM. Notably, this approach is useful to model adverse conditions, such as in the case of a sharp adjustment of asset valuations due to a stressful climate transition shock.13

2.2.1. Extending Hałaj’s (2018) agent-based model

The ABM we develop in this study is based on Hałaj’s (2018, 2020), which explores how liquidity shocks can spread and amplify in the financial system through direct and indirect channels. Hałaj’s (2018) model captures the interactions between banks and asset managers, accounting for feedback effects between liquidity and solvency, as well as the market impact of asset liquidation. Hałaj (2020) calibrates the model using Canadian banking data and simulates various scenarios of funding stress.

In our study, we extend Hałaj’s (2018) ABM to include the other financial system entities within the scope of our study–namely, life insurance companies and pension funds. Further, we fine-tune the calibration of the fire sales parameter to adjust to different financial system entities based on their market liquidity, and we allow different degrees of sensitivity based on a quantile regression estimation.14 We also add a buying behaviour rule for entities with a longer-term investment horizon. These entities would buy assets sold by other entities in the context of a fire sale. And entities would be interested in assets that could transition and become less carbon-intensive or greener (known as climate-transitioning assets). This would imply a positive return in the medium to long run but an initial investment in the short term.

These extensions allow us to explore alternative selling cases to discover insights from different types of market reactions, capturing the stochastic nature of distressed financial periods. The alternative fires sales cases are as follows:

- Base case–baseline parametrization for fire sales in our agent-based model.

- Pension funds actively buy assets–pension funds are assumed to actively buy

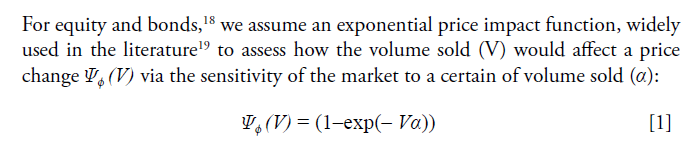

climate-transitioning assets (i.e., those that may help with the climate transition) sold by entities with liquidity needs (investment funds in our framework application). Such assets originate from firms that are not currently benefiting from the transition scenarios but that could benefit over the longer run if a credible transition plan is implemented (i.e., environmental, social and governance [ESG] improvers). The motivation for this case is to reflect the opportunities created by climate-transitioning assets. Pension funds might monitor features related to the fundamental value of firms as well as the credibility of their transition plans. Such “bargain” investments could outperform the market benchmark (i.e., capturing alpha).15 - Amplified fire sales–asset sales, driven by investment funds in our framework application, have a larger effect on falling asset prices, reflecting the non-linearities in the relationship between selling volumes and price changes.16 This could result from, for instance, self-fulfilling panics among investors and precautionary hoarding of liquidity by potential buyers.

2.2.2. Transmission and amplification channels

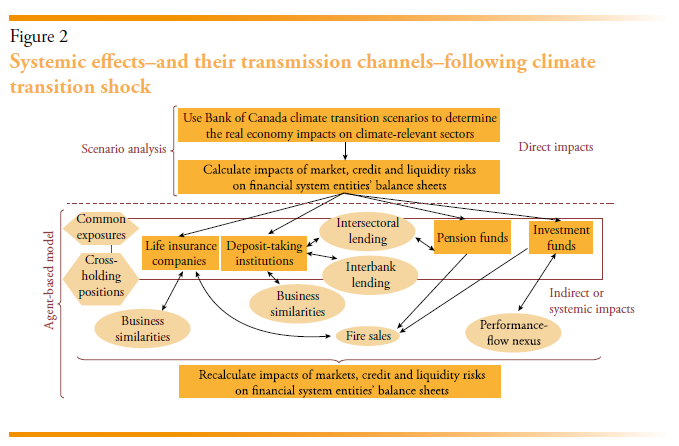

Figure 2 presents an overview of the transmission channels considered in our study.

Common exposures and fire sales

Common exposures can lead to systemic losses when an asset price decreases sharply, either because of a shock to that asset or because of selling pressure in secondary markets, such as in a fire sale. Fire sales could lead to securities being sold at large discounts due to a liquidity shortage. This situation can create opportunities for value investors willing to buy undervalued assets with recovery potential. However, fire sales pose challenges for investors because of increased mark-to-market losses and herd behaviour, potentially leading to larger losses.17

The fire sales are extremely sensitive to the value of α, so as a robustness check, we estimate this value for different types of climate related assets using quantile regression, following Fukker et al. (2022).

Business similarities and funding cost

Moreover, when the asset allocation among financial institutions for a given type of financial entity (e.g., banking sector) is similar, this could indicate potential exposure to similar risks. If an entity faces solvency issues after a shock (such as a climate transition shock), this could be informative about the solvency positions of similar entities, leading to an increase in funding costs.20

In our framework application, we consider how information contagion between entities with similar business models could imply higher funding costs when one entity is facing solvency issues after a climate transition shock. We define a similar business model as firms with similar funding and investment strategies, captured via the cosine similarity. If two firms have a cosine similarity higher than a certain threshold, contagion occurs between financial entities if any of them is facing a higher funding cost due to the solvency deterioration. We follow Hałaj (2018) and set the thresholds of the cosine similarity at 95% for banks, and we assume the same threshold for life insurance companies.

Cross-holding positions

Cross-holding positions refer to entities owning investment (e.g., through shares or debt instruments) in other financial entities. This exposure implies that the financial performance21 of an entity directly influences its investor, thus potentially amplifying losses in the financial system.22

Given each market participant’s asset portfolio, we compute the impacts of the decrease in value of one financial entity into the rest of the financial entities.23 For the debt positions, we follow Hałaj (2018) by focusing on default events without considering the credit deterioration in terms of debt pricing, and by assuming a loss-given-default (LGD) of 40 percent for banks and life insurance companies. Default will occur if the solvency ratio is below the default threshold at any of the steps (or loop) in the ABM after all the previous steps.24

Interbank and intersectoral lending

Lending channels between banks (i.e., interbank lending) or between banks and pension funds (i.e., intersectoral lending) keep liquidity flowing in the financial system. If a lender faces liquidity constraints, this could curtail the lending facilities to other counterparties. The borrower would carry a cost of replacement of the discontinued funding sources.

When banks and pension funds cannot obtain sufficient liquidity from eligible assets, they cease rolling over credit in the interbank and intersectoral lending markets. The debtor then seeks alternative lenders, incurring a search cost as an externality.

Performance-flow nexus

The performance-flow nexus is an amplification channel specific to open-ended mutual funds. Large redemptions, triggered by the poor performance of funds,25 may drive fund managers to sell assets at lower prices to cover withdrawals, burdening remaining investors. This creates a “first-mover advantage” and triggers herding behaviour, which makes it difficult for fund managers to meet all redemption requests. Thus, losses can lead to redemptions, which in turn result in further losses.

Hałaj (2018) captures the non-linear relationship as a redemption of 3% when the change in AuM is below- 6%. We estimate the relationship between weekly flows and returns change for different quantiles for equity funds, bond funds and other funds. The literature has point out to differences between equity and bonds funds in terms of flows,26 which motivate the calibration in terms of the type of mutual fund.

3. Applying the framework using Canadian financial system data

We use Canadian financial system data to apply the methodological framework presented in section 2. This application reveals the types of metrics the framework can generate. These metrics range from initial exposures to more complex financial risk and sectoral interconnectedness measures, both before

and after the climate transition shock occurs.

For this application, we leverage the impacts of the year 2050 for the delayed scenario described in section 2, which is, on average, the most financially stressful. Impacts in 2050 are compared with the baseline scenario.

3.1. Data, assumptions, and limitations

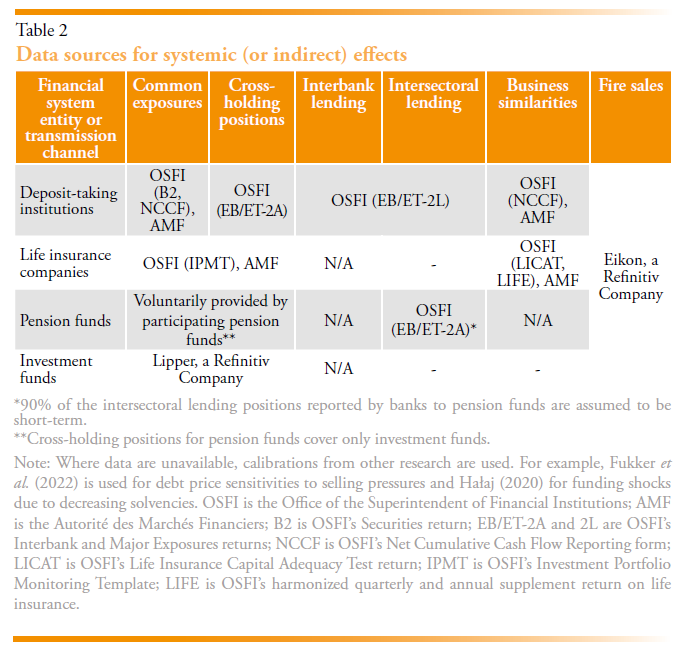

3.1.1. Data sources

We rely on a variety of data sources to capture representative datasets of four major types of financial entities: deposit-taking institutions, life insurance companies, pension funds and investment funds.

The data collection process is multifaceted, involving reliance on various sources and arrangements.

- We use regulatory returns from OSFI for federally regulated deposit-taking institutions and life insurance companies; data for these entities regulated in the province of Quebec are obtained through a data sharing agreement with the AMF.

- Collaboration with several Canadian pension funds and asset managers of pension funds allows us to acquire detailed data on their exposures to climate-relevant sectors, covering both long and short positions in their portfolios of public and private assets and derivatives.

- For investment funds, we use data from a third-party provider, Lipper, a Refinitiv Company. These data include information on approximately 2,000 open-ended mutual funds and exchange-traded funds (ETFs) in Canada.

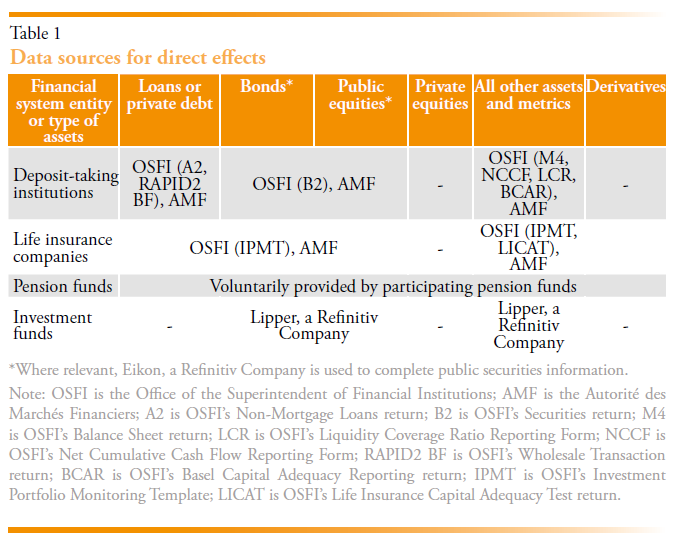

All entities and funds we consider are based in Canada, though as previously mentioned, the analysis includes a worldwide coverage of their assets.27 Table 1 presents the data sources used in the scenario analysis to examine the direct effects of climate transition risk on distinct financial entities. The ABM model was calibrated using some of the data sources described above as well as others. Table 2 provides further details.

3.2. Illustration

The following charts and tables illustrate the potential climate-relevant exposures, vulnerabilities, and risks to the distinct financial system entity types as well as to the financial system as a whole. We explore these features before and after the materialization of the climate transition shock.

3.2.1. Before climate transition shock

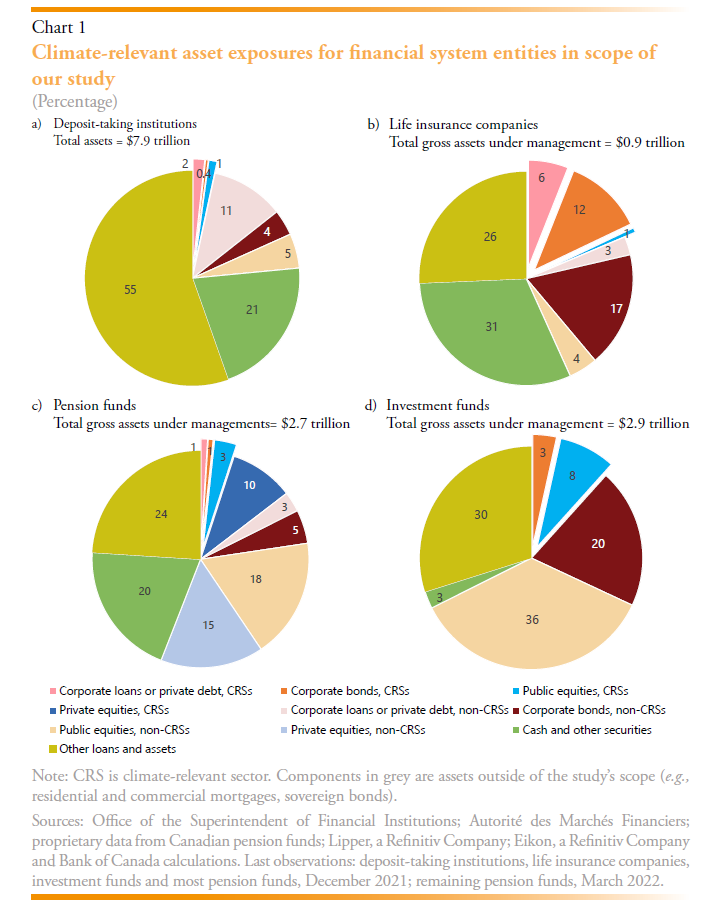

Panels a to d in chart 1 show the initial exposures of climate-relevant assets for the financial system entities within the scope of our study, which collectively manage a substantial portion of the Canadian financial system (total assets approximately $14.5 trillion). These climate-relevant exposures include assets of the following types:

- loans or private debt

- bonds

- public equity

- private equity (for pension funds only)

The financial system’s overall climate-relevant exposures within the scope of our study constitute about 8% of total assets. However, exposures vary across the different types of entities. For instance, deposit-taking institutions have under 4% exposure to climate-relevant assets, while life insurance companies have about 19%.

Exposures also vary across different types of entities in terms of their asset allocations. While life insurance companies tend to have a higher allocation in climate-relevant bonds and loans, pension funds’ and investment funds’ portfolios contain more climate-relevant equities, with pension funds holding a significant amount of climate-relevant private equities.

3.2.2. After climate transition shock (framework application)

The charts in this section show the results from applying our methodological framework. These charts illustrate findings on both the direct effects (through scenario analysis) and systemic effects (through agent-based modelling) after the climate transition shock has occurred. Recall that the shock used in this study originated from the most stressful climate transition scenario–the below 2 °C delayed scenario. The shock’s impacts shown in the charts in this section are relative to the baseline scenario (2019 policies).

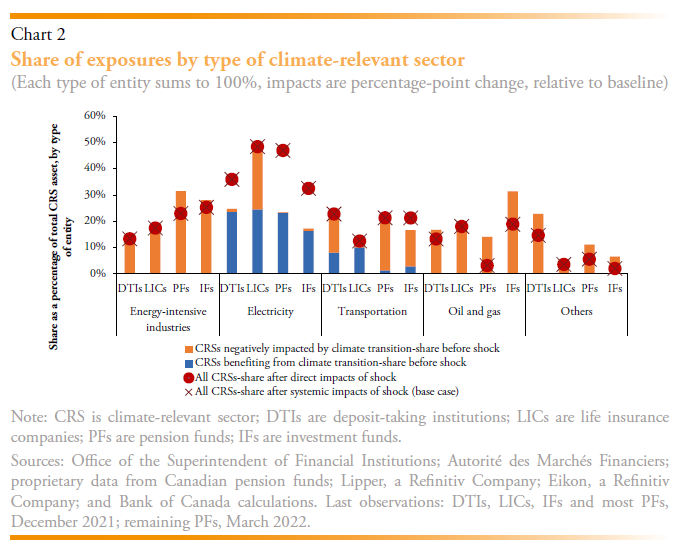

Investment allocation across climate-relevant sectors

Chart 2 presents the asset allocations across climate-relevant sectors for each type of financial entity. The grey and tan bars show the initial share of climate-relevant sector assets before the climate transition shock. Deposit-taking institutions, life insurance companies and pension funds exhibit similar asset allocations in sectors that benefit from our transition scenarios, with about one-third of their climate-relevant assets invested in these sectors. In contrast, investment funds have the smallest stake in these sectors, with less than one-fifth of their climate-related assets allocated in these sectors.

Chart 2 also shows how both the direct effects (red circles) and systemic effects (red Xs) of the climate transition shock can change the weighting of climate-relevant sectors relative to the total climate-related holdings of different financial entity types. Because we assume static balance sheets, changes to asset valuations in each sector after the shock change the relative weight of that sector in the entities’ portfolios. As asset valuations fluctuate because of the shock, the shares of exposures to sectors that benefit from the transition scenarios increase. This is the case for deposit-taking institutions, life insurance companies and pension funds in the electricity sector. However, despite their important exposure to this sector, life insurance companies’ shares increase less than those of pension funds, given that life insurance companies invest more heavily in bonds. Bonds generally fluctuate less in our transition scenarios compared with equities, which are more sensitive to changes in expected future cash flows and discount rates (shown later in chart 5, panel b).

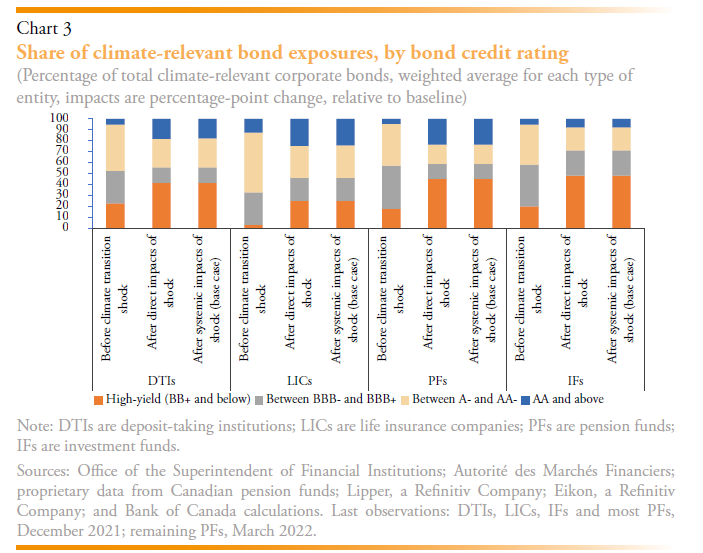

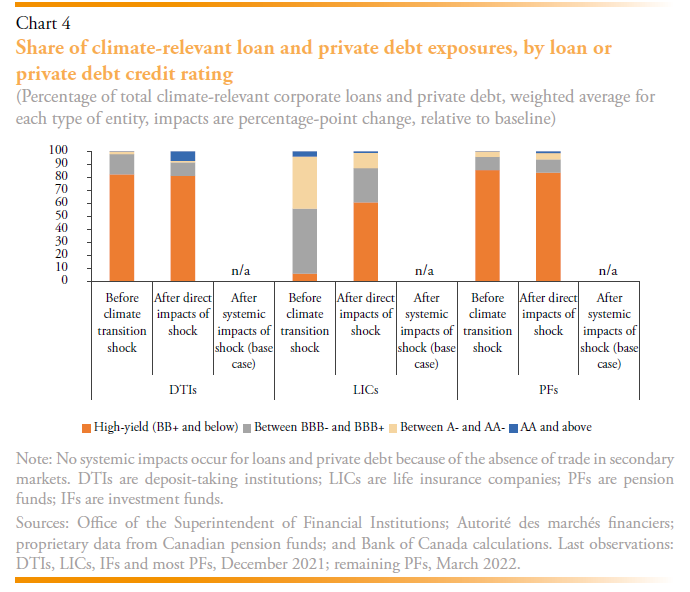

Allocation of debt holdings by credit rating

Financial entities’ risk-taking behaviour concerning their climate-relevant assets also sheds light on the potential effects of a climate transition shock.28 Chart 3 and chart 4 illustrate the role of this informative dimension for climate-relevant bonds as well as climate-relevant loans and private debt. Life insurance companies hold 95% of their pre-shock climate-relevant bonds and loans allocation in the investment-grade space. Pension funds, meanwhile, exhibit a riskier pre-shock investment profile, with a significant portion of their climate-relevant private debt falling into the high-yield space.29 Investment funds also hold a notable percentage of their climate-relevant corporate bond portfolio in high-yield securities.

Charts 5 and 6 also show that the allocation of credit risk becomes riskier as the climate-relevant bonds and loans are negatively impacted by the climate transition shock, migrating from investment-grade to the high-yield credit rating (shown in the charts by the increasing length of the red bars after the climate shock). This is particularly evident in the average risk profile of climate-relevant bond portfolios of pension funds and investment funds. Conversely, the credit ratings of climate-relevant assets in those sectors that stand to benefit from the transition see an improvement following the direct impacts (shown by the increasing length of the green and blue bars in chart 3 and chart 4). This is particularly noteworthy for all entity types except investment funds, given their exposure to sectors that benefit from the transition.

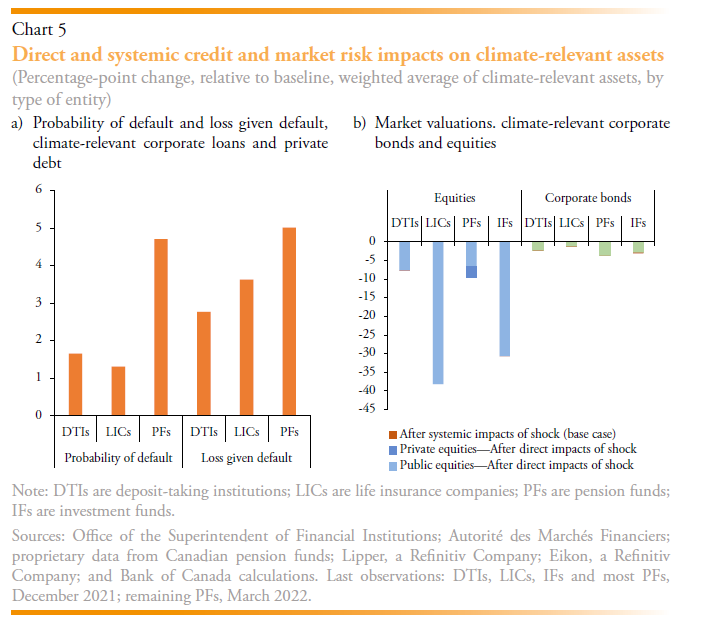

Credit, market and liquidity risk impacts

Chart 5 shows the direct effects on credit and market risks for the portfolios held by financial system entities after the climate transition shock. Deposit-taking institutions face a notable increase in credit risk in their climate-relevant loans portfolio (chart 5, panel a). Their climate-relevant equities also experience significant market valuation impacts, while the effects on bonds are relatively minor (chart 5, panel b). However, as we show later, the valuation of total assets in deposit-taking institutions’ portfolios are not materially affected due to their relatively low initial exposure to climate-relevant assets.

Life insurance companies experience lower credit risk impacts than deposit-taking institutions, which is consistent with their allocation of climate-relevant assets and risk-taking behaviour. Moreover, despite a considerable decrease in equity valuations, the overall impact is small due to life insurance companies’ limited investment in climate-relevant equities. Pension funds’ riskier investment profile contributes to the potential for greater losses, with a substantial increase in the average probability of default on their climate-relevant private debt portfolio. However, they face a relatively smaller decline in their average climate-relevant equity valuations, primarily from their public equity portfolio. Like other entities, investment funds show moderate credit risk impacts but face significant decline in their equity valuations.

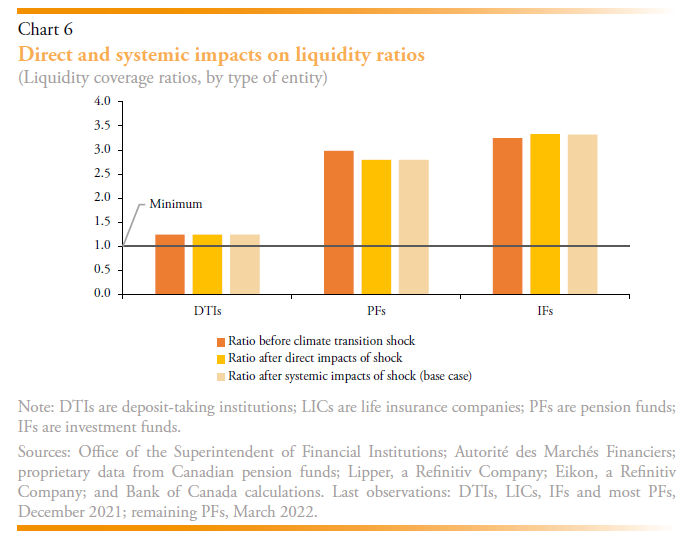

A financial system’s vulnerability to a climate transition shock may also be informed by impacts on the liquidity ratios of the different entities. Chart 6 assesses how the liquidity ratio is impacted by the revaluation of assets, and in the specific case of pension funds, by the losses and margin calls from their derivatives exposures. It shows that liquidity ratios for all types of financial entities remain, on average, well above the threshold for the liquidity coverage ratio for deposit-taking institutions or expected outflows for pension funds and investment funds. This suggests that the financial entities have adequate liquidity to meet their obligations and cope with potential shocks.

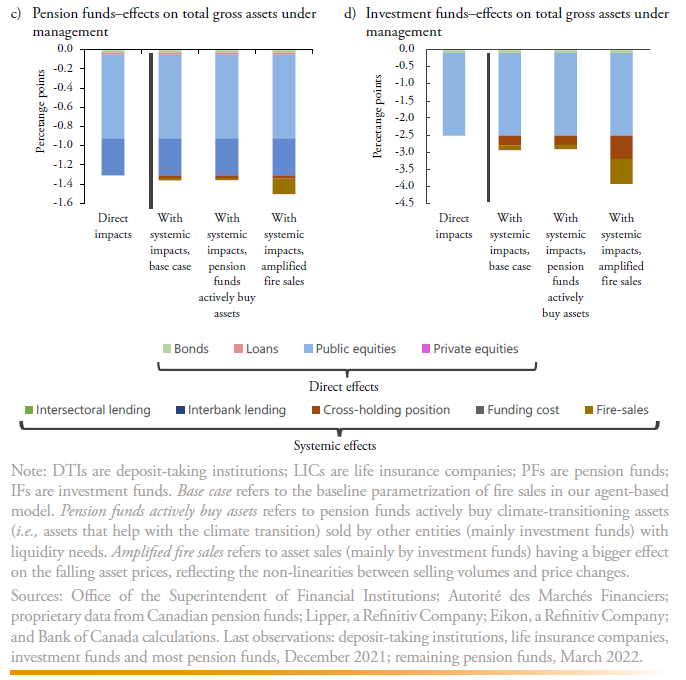

Asset valuation impacts by transmission channel

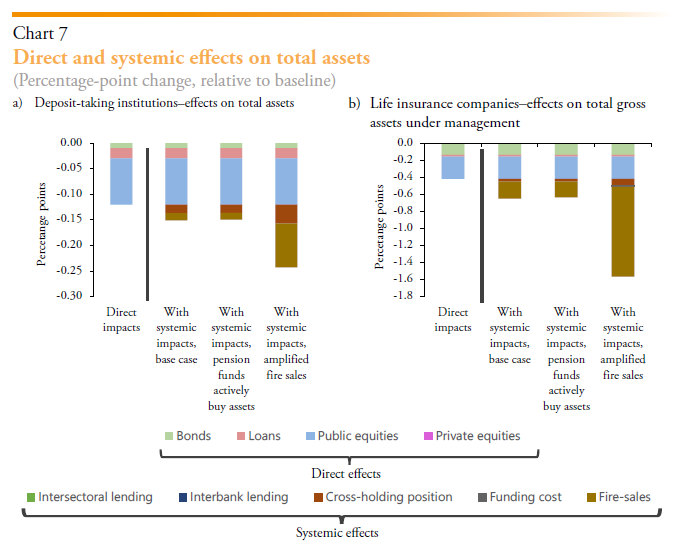

The panels in chart 7 show the changes in total asset valuations for different financial entities’ portfolios. For deposit-taking institutions, life insurance companies and pension funds, the total asset valuations experience a minor to milder decline after the direct effects of the climate transition shock (first column in all panels). The deposit-taking institutions’ relatively low initial exposure to climate-relevant assets, and life insurance companies’ and pension funds’ diversified portfolios, help mitigate direct impacts. Investment funds, in contrast, face greater direct effects, with a notable decline in their total gross assets under management, especially for equity funds.

Though we observe mild direct effects of the climate transition shock, systemic effects may amplify these initial losses. To provide insights around this finding, the panels in chart 7 also present the transmission channels under the three alternative fire sale cases discussed in section 2:

- base case–baseline parametrization for fire sales in our agent-based model,

- pension funds actively buy assets–pension funds actively buy climate-transitioning assets (i.e., assets that may help with the climate transition) sold by investment funds facing liquidity needs,

- amplified fire sales–asset sales (mainly by investment funds) have a bigger effect on the falling asset prices, reflecting the non-linearities between selling volumes and price changes.

Our analysis shows that even in the base case, mild direct effects–mostly triggered by fire sales–can increase significantly when accounting for these channels. While pension funds can lessen systemic effects through their active buying, the purchases are not large enough to absorb all undervalued assets. Finally, in the amplified fire sales case, the fallout from fire sales is significantly larger, triggering an increase in funding costs for life insurance companies and doubling the impact on investment funds’ cross-holding positions.

4. Conclusion

We developed a methodological framework to understand the propagation of shocks across the financial system. This framework uses an agent-based model informed by risks scenario analysis, providing insights into the direct effects and systemic implications of various shocks. We applied this framework to Canadian financial system data in the context of the materialization of a climate transition risks.

Our application reveals how different financial entities are impacted by shocks, considering factors such as exposure to relevant assets, risk-taking behavior, size, investment horizon, business models, and asset mixes. This approach shows that while systemic factors can amplify the direct effects of shocks, assessing initial exposures provides valuable insights into the risks faced by financial entities. Evaluating portfolio allocations by sector and asset type highlights how some entities may be less susceptible to shocks due to their exposure to beneficial sectors.

The size of a financial entity significantly influences its ability to understand and adapt to shocks. Larger entities, with more diversified portfolios and advanced risk assessment capacities, are better equipped to navigate challenges. Other factors, such as risk management strategies, sectoral focus, and regulatory environment, also play crucial roles.

Investment horizons are another critical factor. Entities with long investment horizons, like pension funds and life insurance companies, may act as stabilizers during shocks due to their long-term focus. In contrast, deposit-taking institutions and investment funds, with shorter investment horizons and more fragile funding sources, may increase volatility in fire-sale environments.

Our analysis also highlights how shocks can spread across entity types, potentially creating systemic implications. Common exposures reveal the degree of portfolio interconnectedness in the financial system. Despite low initial direct exposures, transmission channels like cross-holding positions and fire sales can amplify direct effects. Some entities, such as investment funds, are more likely to propagate shocks, while others, like pension funds, act as shock absorbers.

Our findings underscore the need for further analytical efforts encompassing a broader range of asset types and sectors. This will provide a more comprehensive understanding of financial risks across the landscape. Our work strengthens knowledge of how distinct financial entities may be impacted by and respond to financial risks and opportunities, and the potential channels through which these risks and opportunities may spread. More broadly, our work contributes to building standardized systemic risk assessment and monitoring tools.

References

Abad, J., D’Errico, M., Killeen, N., Luz, V., Peltonen, T., Portes, R., and Urbano, T. (2022). Mapping Exposures of EU Banks to the Global Shadow Banking System. Journal of Banking & Finance, 134, 106168.

Acemoglu, D., Ozdaglar, A., and Tahbaz-Salehi, A. (2015). Systemic Risk and Stability in Financial Networks. American Economic Review, 105(2), 564–608.

Acharya, V. V., and Yorulmazer, T. (2008). Information Contagion and Bank Herding. Journal of Money, Credit and Banking, 40(1), 215–231.

Ahnert, T., and Georg, C-P. (2018). Information Contagion and Systemic Risk. Journal of Financial Stability, 35(C), 159–171.

Aikman, D., Chichkanov, P., Douglas, G., Georgiev, Y., Howat, J., and King, B. (2019). System-wide stress simulation. Bank of England Staff Working Paper, No. 809.

Altman, E. I., Brady, B., Resti, A., and Sironi, A. (2005). The link between default and recovery rates: Theory, empirical evidence, and implications. The Journal of Business, 78(6), 2203-2228.

Altman, E. I., and Kalotay, E. A. (2014). Ultimate recovery mixtures. Journal of Banking & Finance, 40, 116-129.

Arora, R., Bédard-Pagé, G., Ouellet Leblanc, G., and Shotlander, R. (2019). Bond Funds and Fixed-Income Market Liquidity: A Stress-Testing Approach. Bank of Canada Technical Report, No. 115.

Arora, R., and Ouellet Leblanc, G. (2018). How Do Canadian Corporate Bond Mutual Funds Meet Investor Redemptions? Bank of Canada Staff Analytical Note, No. 2018-14.

Bardoscia, M., Barucca, P., Battiston, S., Caccioli, F., Cimini, G., Garlaschelli, D., Saracco, F., Squartini, T., and Caldarelli, G. (2021). The physics of financial networks. Nature Reviews Physics, 3(7), 490-507.

Barucca, P., Mahmood, T., and Silvestri, L. (2021). Common asset holdings and systemic vulnerability across multiple types of financial institution. Journal of Financial Stability, 52, 100810.

Battiston, S., Mandel, A., Monasterolo, I., Schütze, F., and Visentin, G. (2017). A climate stress-test of the financial system. Nature Climate Change, 7(4), 283-288.

Bédard-Pagé, G., Bolduc, D., Demers, A., Dion, J. P., Pandey, M., Berger-Soucy, L., and Walton, A. (2021). COVID-19 crisis: Liquidity management at Canada’s largest public pension funds. (No. 2021-11). Bank of Canada Staff Analytical Note.

Caccioli, F., Ferrara, G., and Ramadiah, A. (2020). Modelling fire sale contagion across banks and non-banks (No. 878). Bank of England.

Calimani, S., Hałaj, G., and Żochowski, D. (2022). Simulating fire sales in a system of banks and asset managers. Journal of Banking & Finance, 138, 105707.

Cetorelli, N., Duarte, F. M., and Eisenbach, T. M. (2016). Are asset managers vulnerable to fire sales? (No. 20160218). Federal Reserve Bank of New York.

Chrétien, E., Darpeix, P., Gallet, S., Grillet-Aubert, L., Lalanne, G., Malessan, A., Novakovic, M., Salakhova, D., Samegni-Kepgnou, B., and Vansteenberghe, E. (2020). Exposures through common portfolio and contagion via bilateral cross holdings among funds, banks and insurance companies. Haut Conseil de Stabilitè Financière Working Papers.

Chen, Y.-H. H., Ens, E., Gervais, O. Hosseini, H., Johnston, C., Kabaca, S., Molico, M., Paltsev, S. Proulx, A., and Toktamyssov, A. (2022). Transition Scenarios for Analyzing Climate-Related Financial Risk. Bank of Canada Staff Discussion Paper No, 2022-1.

Chernenko, S., and Sunderam, A. (2016). Liquidity Transformation in Asset Management: Evidence from the Cash Holdings of Mutual Funds. National Bureau of Economic Research Working Paper, No. 22391.

Cifuentes, R., Ferrucci, G., and Shin, H. S. (2005). Liquidity risk and contagion. Journal of the European Economic Association, 3(2-3), 556-566.

Cont, R., and Schaanning, E. (2017). Fire sales, indirect contagion and systemic stress testing. Indirect Contagion and Systemic Stress Testing (June 13, 2017).

Cont, R., Kotlicki, A., and Valderrama, L. (2020). Liquidity at risk: Joint stress testing of solvency and liquidity. Journal of Banking & Finance, 118, 105871.

Dötz, N., and Weth, M. A. (2019). Redemptions and Asset Liquidations in Corporate Bond Funds. Deutsche Bundesbank Discussion Paper, No. 11/2019.

Douglas, G., and Roberts-Sklar, M. (2018). What drives UK defined benefit pension funds’ investment behaviour? Staff Working Paper, No. 757.

Duarte, F., and Eisenbach, T. M. (2021). Fire‐sale spillovers and systemic risk. The Journal of Finance, 76(3), 1251-1294.

Dubiel-Teleszynski, T., Franch, F., Fukker, G., Miccio, D., Pellegrino, M., and Sydow, M. (2022). System-wide amplification of climate risk. ECB Macroprudential Bulletin, 17.

European Securities and Markets Authority. (ESMA). (2015). Measuring the Shadow Banking System – A Focused Approach. In Report on Trends, Risks and Vulnerabilities, No. 2, 2015 34–38.

European Securities and Markets Authority. (ESMA). (2019). Stress Simulation for Investment Funds. ESMA Economic Report.

Fricke, C., and Fricke, D. (2021). Vulnerable asset management? The case of mutual funds. Journal of Financial Stability, 52, 100800.

Fukker, G., Kaijser, M., Mingarelli, L., and Sydow, M. (2022). Contagion from market price impact: A price-at-risk perspective (No. 2692). European Central Bank.

Goldstein, I., Jiang, H., and Ng, D. T. (2017). Investor Flows and Fragility in Corporate Bond Funds. Journal of Financial Economics, 126(3), 592–613.

Gourdel, R., and Sydow, M. (2023). Non-banks contagion and the uneven mitigation of climate risk. International Review of Financial Analysis, 89, 102739.

Hałaj, G. (2018). System-Wide Implications of Funding Risk. Physica A: Statistical Mechanics and its Applications, 503, 1151–1181.

Hałaj, G. (2020). Resilience of Canadian banks to funding liquidity shocks. Latin American Journal of Central Banking, 1(1-4), 100002.

Hosseini, H., Johnston, C., Logan, C., Molico, M., Shen; X., and Tremblay, M.-C. (2022). Assessing Climate-Related Financial Risk: Guide to Implementation of Methods. Bank of Canada Technical Report, No. 120.

Huang, J. (2020). Dynamic Liquidity Preferences of Mutual Funds. Quarterly Journal of Finance, 10(4), 2050018.

Johnston, C., Vallée, G., Hosseini, H., Lindsay, B., Molico, M., Tremblay, M.-C., and Witts, A. (2023). Climate-Related Flood Risk to Residential Lending Portfolios in Canada. Bank of Canada Staff Discussion Paper, No. 33.

Lux, T., and Zwinkels, R. C. J. (2018). Empirical Validation of Agent-Based Models. In C. Hommes and B. LeBaron (eds.), Handbook of Computational Economics (Vol. 4) (437–488). Oxford, United Kingdom: Elsevier.

Mirza, H., Moccero, D., Palligkinis, S., and Pancaro, C. (2020). Fire sales by euro area banks and funds: What is their asset price impact? Economic Modelling, 93, 430-444.

Ojea-Ferreiro, J. (2020). Quantifying Uncertainty in Adverse Liquidity Scenarios for Investment Funds. CNMV Bulletin Quarter, II, 25–44.

Puhr, M. C., Santos, M. A., Schmieder, M. C., Neftci, S. N., Neudorfer, M. B., Schmitz, M. S. W. and Hesse, M. H. (2012). Next generation system-wide liquidity stress testing. International Monetary Fund.

Schnabel, I., and Shin, H. S. (2002). Foreshadowing LTCM: the crisis of 1763, No 02-46, Papers, Sonderforschungsbreich 504.

Sydow, M., Schilte, A., Covi, G., Deipenbrock, M., Del Vecchio, L., Fiedor, P., Fukker, G., Gehrend, M., Gourdel, R., Grassi, A., and Hilberg, B. (2021). Shock amplification in an interconnected financial system of banks and investment funds.

Wang, D., van Lelyveld, I., and Schaumburg, J. (2019). Do Information Contagion and Business Model Similarities Explain Bank Credit Risk Commonalities? European Systemic Risk Board Working Paper Series, No. 9

NOTES

* Financial Stability Department, Bank of Canada. Bank of Canada staff working papers provide a forum for staff to publish work-in-progress research independently from the Bank’s Governing Council. This research may support or challenge prevailing policy orthodoxy. Therefore, the views expressed in this paper are solely those of the authors and may differ from official Bank of Canada views. No responsibility for them should be attributed to the Bank. (bankofcanada.ca; GBruneau@bankofcanada.ca; JOjeaFerreiro@bankofcanada.ca; APlummer@bankofcanada.ca; MTremblay@bankofcanada.ca; AWitts@bankofcanada.ca).

♦ We thank Thibaut Duprey, Ruben Hipp and Miguel Molico for their helpful comments and discussion. We also thank Grzegorz Hałaj for his support and guidance in earlier phases of this work. We are grateful to Alper Odabasioglu for his generous support, expert advice and comments. We truly appreciate the valuable support from Michele Sura and Monique Ménard. We also extend our thanks to Adam Su, Miguel Jutras, Shamanth Chedde and James Younker for their assistance in the treatment of the different data sources. Finally, we thank several organizations for voluntarily sharing their data and for the insightful discussions, including the Office of the Superintendent of Financial Institutions; Autorité des marchés financiers; Financial Services Regulatory Authority of Ontario; Air Canada Pension Master Trust Fund; Alberta Investment Management Corporation (AIMCo); British Columbia Investment Management Corporation (BCI); CAAT Pension Plan; Canada Post Corporation Registered Pension Plan; CPP Investments; Caisse de Dépôt et placement du Québec (CDPQ); Desjardins Sécurité Financière, compagnie d’assurance-vie; Fédération des Caisses Desjardins du Québec; Healthcare of Ontario Pension Plan; iA Groupe financier/iA Financial Group; Investment Management Corporation of Ontario; OMERS Administration Corporation; OPSEU Pension Plan Trust Fund (OPTrust); Ontario Teachers’ Pension Plan (OTPP); Public Sector Pension Investment Board (PSP Investments); Suncor Energy Pension Plan; TD Bank Group; and University Pension Plan (UPP). We would also like to thank seminar participants at Oxford Climate Econometrics Seminar and at the Spanish National Securities Market Commission (CNMV), and participants at the 2024 Latin American Journal of Central Banking (LAJCB) conference, the XIX conference of the Spanish association for Energy Economics (AEEE), the 2024 Annual Meeting of the Commodity and Energy Markets Association (CEMA), the 58th Annual Meetings of the Canadian Economics Association (CEA), the Agent-Based Modelling for Policy (ABM4Policy) workshop organized by Bank of England, and the 2024 Annual Meeting of the Société Canadienne de Science Économique (SCSE). Previous versions of this work have benefited from discussions within the FSB and IMF groups of which the Bank is a member.

1 Many financial authorities around the world have adopted scenario analysis to support their analysis of the macroeconomic and financial impacts of climate change. See Network for Greening the Financial System (2021).

2 For more information on the four Bank of Canada climate transition scenarios and a list of regions covered, see Bank of Canada and OSFI (2022) and Chen et al. (2022).

3 For the list of climate-relevant sectors and a mapping to the most widely used industrial classification, see Bank of Canada and OSFI (2022).

4 For example, direct emissions costs for a sector may increase due to the sector’s efforts to reduce greenhouse gas emissions. Indirect costs faced by a sector are those that are passed on from other sectors upstream. Capital expenditures, in turn, may rise with investment in new technologies. And the climate transition could lead to changes in consumer preferences, which may result in decreased demand and lower revenues for some firms.

5 In the context of the Bank–OSFI pilot project, the risk assessments focused on Canada and the United States since these two countries accounted for most of the assets of the pilot participants. Considering the larger scope of financial institutions in our study, we extend these risk assessments to all regions covered by the climate transition scenarios.

6 The credit risk assessment method follows the methodology described in United Nations Environment Programme Finance Initiative (UNEP-FI), Oliver Wyman and Mercer, “Extending Our Horizons–Assessing credit risk and opportunity in a changing climate: Outputs of a working group of 16 banks piloting the TCFD Recommendations,” (April 2018). In the pilot project, participating financial institutions were asked to select a minimum of five representative borrowers per sector in their portfolios. This choice balanced the benefits of higher precision in the estimated climate transition–credit risk relationship and the cost of the assessments for the financial institutions. For more details on the methodological steps taken in the

pilot’s credit risk assessment, see Hosseini et al. (2022) and Bank of Canada and OSFI (2022).

7 Region-sector equity index values were estimated by discounting computed annual dividend flows within a 50 year, forward-looking window for each of the three climate transition scenarios from 2020 to 2100.

8 Dividends were discounted using Morgan Stanley Capital International’s average historical returns. See Hosseini et al. (2022) and Bank of Canada and OSFI (2022) for more details on the market risk assessment approach.

10 See Bank for International Settlements (2013).

11 See Bédard-Pagé et al. (2021).

12 Notably, we exclude profit maximization based on balance sheet optimization, leverage

ratio, or ALM measures, as our focus remains on short-term horizons.

13 ABMs are well suited to capture stylized facts of the financial system, including periods of turmoil (e.g., out-of-equilibrium behaviours, multiple decision rules, heterogeneous and disaggregated balance sheets, and non-linear dynamics and spillovers). But it is worth noting a few of the drawbacks of ABMs. One drawback relates to parameter calibrations, where historical data may not be accurate depictions of actual values, which might not yet be observed. Another drawback is the stability of the model, which is highly dependent on the parameter selection. For more details on ABMs, see Lux and Zwinkels (2018).

14 This follows Fukker et al. (2022).

15 We reflect this investment possibility for pension funds to capture the effects of such an investment strategy, which may smooth out the burden related to the market stress faced by the financial system.

16 See Fukker et al. (2022).

17 Common exposures can have positive effects in normal times, such as diversification benefits and risk sharing. But they can also have negative effects in downturns through the amplification of losses and contagion. These effects can have adverse consequences for the real economy by reducing credit availability, investment opportunities and consumer confidence. See, for example, Acemoglu, Ozdaglar and Tahbaz-Salehi (2015) and Abad et al. (2022).

18 Price change in bonds would change the interest rate, making an effect on balance sheet no matter the FI is selling or not the bond. Drop in prices would constraint the funding opportunities of the issuer company, implying a higher yield and a higher credit risk due to this restriction.

19 See, for instance, Schnabel and Shin (2002), Cifuentes et al. (2005), Cont and Schaanning (2017).

20 Borrower default risk can also inform lender solvency risks (see Ahnert and Georg [2018]) and other lenders’ solvency situations if a common systematic factor is shared (see Acharya and Yorulmazer [2008]). See Wang, et al. (2019) for a discussion of information contagion through business model similarities.

21 The equity returns are built for banks and life insurance companies based on their percentage change in equity value, while for the investment funds we compute the change in the total assets under management (AuM).

22 Although we model mutual funds as active players, we consider the whole investment fund sector, as they would play a passive role in terms of cross-holding contagion, without taking any active in relation with liquidity measures.

23 However, the coverage is not perfect. We can get the positions of investment funds in participations or equity shares in other investment funds, banks and life insurance companies. For life insurance companies, we can capture banks, other life insurance companies and investment funds. For banks, the investment in other market participants is limited to the DSIBs through the EBET-2A returns, but no information is available for SMSBs. Finally, the positions of pension funds is only known for investment funds, being the coverage we were able to capture quite diverse depending on the pension fund.

24 Note that default will be also translated into a lender search for the borrowers in the intersectoral and interbanking sectors, implying a search cost, as described in steps 2 and 3.

25 This channel has been observed in corporate bond funds (Goldstein et al., 2017; Dötz and Weth, 2019) and equity funds (Chen et al., 2010). The performance-flow nexus has been introduced in several resilience exercises for mutual funds (Arora and Ouellet Leblanc, 2018; ESMA, 2019; Gourdel and Sydow, 2022; Ojea-Ferreiro, 2020; Fricke and Fricke, 2021).

26 See, for instance, Goldstein et al. (2017); Dötz and Weth (2019) and Chen et al. (2010).

27 Our study presents results for Canadian-domiciled open-ended mutual funds and ETFs. The mutual funds and ETFs are limited to equities, bonds, mixed assets, and others (including alternatives, money markets). Funds with asset compositions like real estate and commodities are outside the scope of our study. The ABM model includes investment funds domiciled in Canada, the United States or abroad that received investment from a Canadian financial entity. The inclusion of foreign entities intensifies market selling pressure, amplifying the fire sale effects.

28 In this study, the riskiness of an asset is based on its credit rating. Higher credit ratings indicate lower risk and higher credit quality, while lower credit ratings indicate higher risk and lower credit quality.

29 This corroborates a trend that indicates pension funds are taking more risk in private markets. However, through the negotiation of covenants, pension funds have a tighter hold on the terms of private debt contracts. For example, contract terms may incorporate details around a firm’s climate transition plans, serving to mitigate climate-related risk.